Electricity is the backbone of any economy and one of the necessities of modern life. Since even before the current war, poor electricity services in Yemen have been one of the key barriers to sustainable economic development and basic service provisions, such as water supply, health care, and education.

This policy brief presents an overview of the electricity sector and its relevant indicators prior to the conflict. It then outlines the impact of the conflict on the sector, and concludes with a set of priorities for restoring the pre-war capacity of the electricity sector, then further reforming it to improve its performance.

Immediate- to short-term recommendations include: adopting a realistic and practical recovery plan; securing funds for rehabilitating the infrastructure; reviewing the electricity tariff; reducing technical and non-technical electricity losses; purchasing electricity when needed through a competitive process and via least-cost options, such as gas and renewable energy; securing the fuel supply and the salaries of sector staff; resuming all suspended projects; finding sustainable and feasible solutions for the electricity supply in each governorate to avoid the challenges associated with the centralized grid; and installing sustainable stand-alone solar systems, compatible for connection to the national grid (when restored).

The medium- to long-term priorities include specific recommendations under five categories, relating to: the legal and regulatory framework; institutional arrangements; capacity and performance; private sector participation; and technical issues.

This policy brief was developed based on a more detailed research paper published under the same title by Rethinking Yemen’s Economy project in May 25, 2021. The full research paper can be viewed on this the Development Champions Forum website or by clicking on this link.

Background

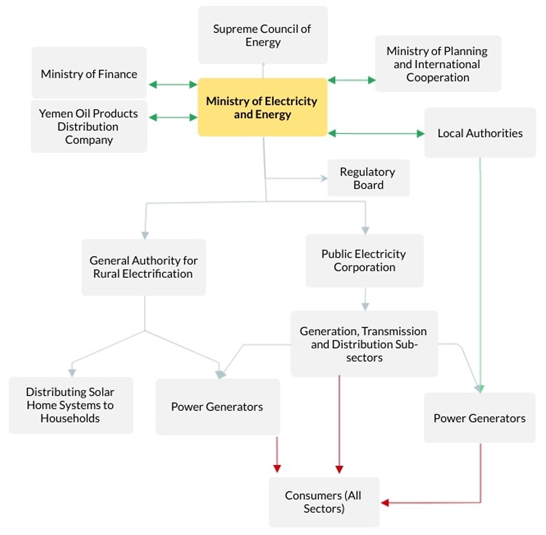

The electricity sector in Yemen is managed by the Ministry of Electricity and Energy (MoEE) which is responsible for setting the sector policies and strategic plans, while the Public Electricity Corporation (PEC) is in charge of electricity provision, managing the electricity sub-sectors of generation, transmission, and distribution. The General Authority of Rural Electrification (GARE), established in 2009, is the body responsible for electrifying specific rural areas that are located outside the main and secondary cities.

The electricity sector activities are governed by Electricity Law No. 1 of 2009. The law stipulated several positive and ambitious measures to reform the sector and improve sector performance, such as unbundling the PEC into three corporate entities – one each for generation, transmission, and distribution – and creating an independent regulator to control sector activities. None of these measures, however, has been achieved to date.

Interrelations Among Key National Stakeholders

Private sector participation in the electricity sector started in 2006 and was limited to electricity generation activities. The PEC purchased the energy from private producers, based on short-term contracts, and supplied them with the fuel needed for generation. The role of the private sector was mainly to back up the PEC in bridging the electricity supply gap. In 2013, the share of purchased energy accounted for around 38 percent of overall generation, while from 2008 to 2012, the average cost of purchased energy represented around 48 percent of sold energy revenues. This indicates that the government – and the power sector in particular – incurred significant financial burdens due to purchased energy from private producers.

Until 2015, the residential sector accounted for most of the country’s electricity consumption, at 65 percent. Given the unreliability of the supply, most of the facilities in the economic sectors, such as commercial and industrial, relied on their own diesel generators as their main source, or as a backup system. In 2012, there were around 2 million subscribers in the electricity sector, and the gap in generation capacity was 376 MW. Due to limited capacity, the unserved energy demand was around 33 percent in 2011 and 25 percent in 2012. Thus, there was a need to disconnect some subscribers at peak times. The electricity tariff was heavily subsidized and was far below the high cost of supply. In 2014, the average cost recovery rate was only 33 percent (as per local market fuel prices).

The Marib I & II gas-fired power plant projects, as well as electricity interconnection projects with neighboring countries, are strategic components of the generation subsector. The Marib I gas power plant was installed in 2009 in Safer, near the gas field, supplying around 50 percent of all Yemen’s generated energy and 40 percent of its actual installed capacity (340 MW). The plant played a crucial role in enhancing generation capacity using the least-cost and locally available resources.

As a second phase, the construction of the 400 MW Marib II began in 2013, with plans to start generation in late 2014. There was also a plan to expand the capacity of Marib I & II by converting them from open-cycle gas turbines to combined cycles. Due to political unrest, the second phase was suspended. Interconnection projects with neighboring countries, namely Saudi Arabia and, via Djibouti, Ethiopia, were under discussion. These projects, however, did not materialize.

Worthy of note, too, is the country’s attempts to utilize renewable energy technologies. Yemen is endowed with significant renewable energy resources, specifically wind, solar and geothermal. Yet, although the National Strategy for Renewable Energy of 2009 set a target of 15 percent renewable energies in the generation mix by 2020, the deployment of renewable energy applications before the war was minimal. The first large-scale wind farm project, of 60 MW, was to be installed in Al-Mokha, funded by several international institutions. Again, due to the war, this project has been suspended.

Wartime Developments

Prior to the war, the installed generation capacity of the electricity sector was significantly low, at 1.5 gigawatts (GW), with the actual capacity only 67 percent of this. The main reason for this low capacity was that most of the key power plants were aging and inefficient. Electricity generation was improving steadily, however, up until 2010, with the 340 MW Marib I gas power plant mentioned above the most recent strategic project. In addition to the limited available generation capacity, losses were substantial, exceeding 40 percent in 2013. This energy loss, combined with a low bill collection rate, a significant tariff subsidy, and the purchase of electricity from expensive sources, were major issues bleeding the sector.

In terms of annual electricity consumption per capita, in 2014, this stood at 255 kWh/year. This was extremely low compared to the regional and international level, where the amounts are 2,900 kWh/year and 3,100 kWh/year, respectively. Due to stunted improvement in electricity expansion, the access rate to public electricity in 2014 was around 40 percent of the population. Furthermore, although the rural areas host around 75 percent of the Yemeni population, the electrification rate in those districts was extremely low, at 23 percent, compared to 85 percent in urban areas.

During the current war, the public electricity sector has been substantially affected by the ongoing armed conflict, suffering considerable physical and non-physical damage. The conflict and the absence of reliable infrastructure have also negatively affected the provision of other basic services, such as health, water, and education. Indeed, it is estimated[1] that during the ongoing war, about 90 percent of the population has not had access to public electricity. In 2020, only 50 percent of health facilities were functioning and they remain negatively affected by power outages up until today[2]. While around 32 percent (303 MW out of 906 MW) of the available capacity of the power plants previously connected to the national grid are still functioning, given the collapse of the grid, those power plants mainly supply local demand.

There is also a divergence between those areas controlled by the internationally recognized government and those controlled by the armed Houthi movement (Ansar Allah), in terms of electricity supply. In the former, supply has remained largely the same; the government-led supply and tariff remain subsidized, with significant reliance on purchased electricity from private producers, and with sporadic fuel grants and support from Saudi Arabia and UAE to address the limited fuel supply. In Houthi -controlled areas, electricity generation has changed to private-led supply. Several private grids are currently providing electricity through small generators.

Since the collapse of the national grid, the solar photovoltaic (PV) market has also boomed at an unprecedented rate, becoming an attainable electricity alternative. This is especially so in the northern and central governorates, where national power plants are not functioning and the price of private electricity is unaffordable for most. In December 2019, around 75 percent of the population used small solar systems as the main source of electricity.

Policy Recommendations

Despite the deteriorating situation in the power sector, especially since the start of the current war, there is an opportunity to build a stronger electricity sector in Yemen.

The following section includes priorities for restoring and reforming that sector. The applicability of these recommendations, however, relies on a highly supportive political environment and the support of international donors/lenders, as well as effective management by sector leaders.

Immediate- to Short-Term

The recommendations below are timed for the current situation and the first year following any potential peace agreement and/or political stability. The aim at this stage is to restore the sector to its previous capacity before the war and prepare a sound foundation for the reform process that must follow the initial recovery phase. The following steps are therefore recommended:

- Adopt a systematic and executable recovery plan for infrastructure rehabilitation priorities in the generation, transmission, and distribution subsectors.

- Secure funds, whether from government financial resources or international donors/lenders, to rehabilitate infrastructure damaged during the war; maintain power plants requiring spare parts; and other corrective and preventive maintenance.

- Rehabilitate essential transmission lines needed to transmit power from large power plants to demand locations. These rehabilitation efforts can be timed in line with the recovery plan.

- Look for effective, financial, and technical solutions/settlements between the relevant parties in the conflict regions to enable the re-starting of the national grid – including the main power plants, such as the Marib I gas power plant, as well as thermal power plants across the governorates.

- Work towards the resumption of all suspended projects and regain the support of international donors.

- Purchase electricity from private producers as needed, via a transparent and competitive process. This would preferably be via schemes that result in the PEC owning the infrastructure, such as build-operate-transfer (BOT) and build-own-operate-transfer (BOOT), when these are feasible, both technically and financially.

- Work towards finding feasible and sustainable solutions for electricity supply in each governorate, both for the current situation and for backup in emergencies when and if the centralized system fails. This may include a demand-need assessment for each governorate. Top priority goes to those governorates/areas that have no generation assets and have thus lost access to electricity since the war started. One of the best options, especially in hot and conflict-affected areas, is to install the least-cost distributed generation systems (i.e., mini-grids), given their operational flexibility and the short time needed for installation.

- Enhance the efficiency of the generation and distribution subsectors; reduce technical losses through proper maintenance; improve the capacity of the overloaded grids’ components; and restore the actual capacity of the power plants. For non-technical losses, it is necessary to reduce unauthorized connections to the grid, increase fee collection and develop the capacity of those who manage the billing and metering. In addition, install prepaid meters.

- Secure sustainable salaries for the electricity sector employees and develop the capacity of the team at all levels and in all fields of specialization: managerial, technical, procurement, etc. This requires assessment and capacity building for the current staff.

- Improve managerial practices and ensure there is an effective delegation of capacities for the skilled and qualified directors/managers who lead the departments/units. This means distributing the responsibilities among different levels of management, setting specific goals, performance indicators, and clear job descriptions. Separate the managerial and financial activities of the three subsectors to enhance accountability and pave the way for restructuring reforms.

- Ensure decision-making autonomy for operations of the electricity sector, especially for those projects that need to be implemented in line with the sector’s strategic plans, or those that require technical and financial feasibility studies.

- Secure sustainable fuel supplies for the power plants through local supplies, imports, and grants.

- Determine the human resources needed and work on re-attracting the well-skilled staff who left during the war. Find replacements for the highly experienced staff who have retired during the past six years, or will retire in the near future.

- Update and benefit from the previous studies and strategies conducted by donors and international consultancy firms, such as the Master Plan, National Strategy for Renewable Energy and the Energy Efficiency[3], and Rural Electrification Strategy.

- Encourage consumers and service facilities to install high-quality and well-designed solar stand-alone systems that are sustainable solutions, as well as connection compatible, once the grid is again operational. This requires surveying the solar PV market, adopting quality specifications and standards, establishing labs for testing, and checking the compliance of imported products, alongside facilitating the importation process and exemption of solar PV products from custom duties in all the country’s ports. The improvement of technical and safety awareness is also necessary, as regards the proper use of solar systems and the disposal of used components, such as batteries, solar panels, and electronic waste.

- Review the electricity tariff based on a consultancy study that addresses its social and economic dimensions, including affordability for consumers from all sectors, demand load forecast, and others. The study should also include a timeline and achievable milestones that aim to reduce the subsidy in those areas where electricity is currently subsidized. If the study advises postponing any increase in the tariff, the government should support the PEC in finding financing channels to help cover the electricity subsidy, in order to meet its operational costs and ensure a reliable electricity supply. There is also a need for social protection mechanisms that target poor people who cannot afford the electricity tariff when the electricity tariff is unsubsidized.

Medium- to Long-Term

These recommendations are applicable during the two- to five-year period following any potential peace agreement and/or political stability. This stage focuses mainly on reforming the sector in accordance with the relevant steps taken before the war and best international practices.

In general, the success of the reform process – especially the restructuring of the sector, the creation of an independent regulator, and the degree of private sector engagement – needs a political commitment translated into an enforceable decree for reform. High-level leaders, supported by a committee of senior experts, should work on initiating, supervising, and directing the reform process so that it obtains stakeholder consensus and ensures smooth reforms leading to the establishment of a modern electricity sector.

Legal and Regulatory Framework

There are a considerable number of important laws and regulations, drafted and/or adapted before the war, that need to be enforced. The reform process can thus build on previous efforts, as well as develop new laws and decrees, to better govern the sector. The following steps are therefore recommended:

- Approve the public-private partnership law drafted before the war, with updates if needed.

- Amend the previous electricity laws as needed, to accommodate new changes in the sector.

- Adopt the necessary supporting policies, regulations, and schemes for engaging the private sector in the electricity generation and distribution sector through BOT and BOOT, among others.

- Approve the renewable energy law, supported by an updated and executable action plan, resources assessment, and mapping. In addition, issue supporting policies, incentives, and schemes to encourage the private sector to invest in clean energy through feed-in tariffs, net metering, auctions, right-to-grid access, and priority of dispatch, among others.

- Reform the electricity tariff and adjust its structure to include, for example, different tariffs by time of use. This may include a gradual removal of the subsidy from the electricity tariff to cover actual costs and generate acceptable level of profit that can sustain operations and investments in the network. In addition, there is a need to ensure that low-income consumers will not be affected negatively by increased tariffs.

- Adopt energy efficiency action plans, including measures to reduce energy consumption in the electricity sector, as well as other sectors. Include specific measures for electrical equipment, buildings, lighting, and minimum energy performance standards and labels for appliances (e.g., air conditioning and refrigerators).

- Adopt a law for sound waste management of electronics, solar panels, and batteries, including procedures of collection and recycling of waste.

- Set a strategic plan that includes milestones towards liberalizing the electricity market through wholesale and retail markets. Appendix 5 of the full research paper presents the phases of competition reform.

- Initiate the reform process through a legally binding document that gives authority to a political leader who can supervise and direct the reform process. This leader, with the support of technical and non-technical experts, needs to enforce the decrees, unify the stakeholder’s opinions, and make sure that the reforms lead to the desired outcomes.

Institutional Arrangement

The Electricity Law of 2009 included the main necessary steps for reforming the structure of the electricity sector. The following points emphasize the importance of enforcing the electricity law, as well as supplementary recommendations:

- Create an independent regulatory entity to ensure an enabling investment environment that can promote fair competition among the stakeholders and protect the consumers. Appendix 3 of the full research paper presents a list of the regulatory performance indicators.

- Resume and build on previous efforts to restructure the General Authority of Rural Electrification and create service providers in the rural areas.

- Unbundle the electricity sector into generation, transmission, and distribution subsectors.

- Set a strategic, executable plan for the horizontal unbundling of the generation and distribution components to liberalize the electricity market.

- Create financial institutions and mechanisms to finance small- and large-scale energy project investments and provide soft loans and subsidies.

Capacity and Performance

Enhancing the capacity of institutions and individuals is key to improving the sector’s performance. Thus, the following steps should be taken:

- Improve the governance and managerial practices of the PEC, such as implementing staff performance reviews as per predefined goals, financial auditing by a third party, ability to hire employees, and firing of poor performance employees, and others. Appendix of the full research paper presents a list of indicators for the utilities’ governance performance.

- Develop innovative solutions to enhance the rural electrification programs. This needs to include accessible financing mechanisms for villagers to buy solar stand-alone systems, as well as mechanisms for investors.

- Enhance the capacity of the electricity sector to deal effectively with donor-supported, large-scale projects, while also attracting new partners and projects. This should include a review of the entire donor collaboration and project implementation processes to ensure timely decisions and their implementation.

- Enhance the capacity of training centers in the electricity sector and ensure staff development across all levels and in all fields.

- Develop the capacity of the technical team to prepare technical and legal documents and regulations, such as standard Power Purchase Agreements (PPA), regulations needed for connecting the renewable energy project to the grid, feasibility studies, and others.

Private Sector Involvement

Perhaps counterintuitively, countries during a conflict or in a post-conflict transition phase have many investment opportunities, usually centered on the provision of unmet basic services and needs. The private sector can play an important role in infrastructure and economic reconstruction, which in turn results in several positive outcomes, such as an increase in private capital and job creation while (re)building local capacities and skills. The private sector also generates revenue for the government by paying taxes and other fees. Therefore, the following measures are recommended:

- Adopt appropriate incentives and arrangements for attracting private sector investments. This especially applies to the technologies that generate clean energy (i.e., from renewable energy sources, namely, the solar, wind, and geothermal energy), or those with competitive prices, such as gas-fired power plants.

- Engage the private sector in the electricity sector’s activities, especially in the generation and distribution sectors, which have significant potential for private sector participation. Appendix 4 of the full research paper presents several arrangements for involving the private sector in the electricity sector.

- Provide fiscal incentives and guarantees to the private sector to minimize possible risks. These include: sovereign guarantees in case of premature contract termination; a take-or-pay clause in the PPA to guarantee the purchase of produced power when there is no demand; and a concerted effort to minimize risk for the private sector, especially in the initial post-war years.

- Allocate land for electricity sector investments, especially for renewable energy projects where there are abundant resources.

Technical

Several technical recommendations are needed to improve the electricity services and their quality. The top technical priorities to enhance the performance of the generation, distribution, and transmission sectors are:

- Improve the quality, reliability, and availability of the electricity supply by regulating the voltage level and reducing the number and period of interruptions.

- Invest in installing power plants in line with previous plans and consider supplying the economic sectors (e.g., industrial and commercial) with a higher share of electricity generation. These sectors, especially energy-intensive industries, rely on electricity generated by diesel generators – an expensive option. Therefore, the cost of electricity produced by the PEC could benefit from the economies of scale of large power plants and generate electricity by least-cost options (i.e., gas), which in turn will be affordable for those sectors.

- Develop the grid code for connecting renewable energy projects to the national grid.

- Work towards the resumption of the interconnection projects with Saudi Arabia and Ethiopia.

- Upgrade, modernize and expand the transmission and distribution infrastructure. One of the main causes of technical losses was overloading the already deteriorated or limited capacity of the electricity infrastructure. Upgrading this network will be an important step towards improving energy efficiency.

- Develop and implement an emergency plan for the electricity supply, to counter unexpected crises and damages to the centralized grid. The plan can include installing distributed generation units in the governorates. Renewable energy power plants are preferred, to avoid the risks to fuel supply, especially during armed conflict and political instability.

Endnotes

- “Overall Socioeconomic Developments,” Yemen Socio-Economic Update 20, Ministry of Planning and International Cooperation (MoPIC), November 2016, https://reliefweb.int/sites/reliefweb.int/files/resources/ yseu20_english_v8_final.pdf (accessed August 7, 2020).

- UN Office for the Coordination of Humanitarian Affairs (OCHA) Yemen, “Yemen Humanitarian Update” (issue 3), March 2020, https://reliefweb.int/report/yemen/yemen-humanitarian-update-issue-3- march-2020-enar (accessed August 7, 2020).

- The summary of the ‘National Strategy for Renewable Energy and the Energy Efficiency’ available at https://moee-ye.com/site-ar/364/