Yemen is one of the most water-scarce countries in the world, with renewable water resources currently capable of providing only 75 m3 per capita per year – well below the water scarcity threshold. And this volume is steadily dropping. The agricultural sector in Yemen is the dominant user of groundwater resources, accounting for around 90 percent of total consumption. Due to the current crisis, fuel required for pumps has become scarce and very expensive; as a result, solar energy has begun to play a role in the extraction and supply of groundwater for irrigation. However, there is concern about the misuse of this new technology. This study examines the current trend of solar-powered irrigation system (SPIS) use in Sana’a Basin, identifying the pros and cons of this approach. It presents the perspectives of farmers and experts in terms of what is happening and what should be done to maximize the benefits and minimize the negative impacts of SPIS. The incidence of SPIS installation is increasing at a rate of more than 4 percent annually. Farmers spoken to as a part of this study expressed enthusiasm to use SPIS and cited capital cost as the biggest obstacle to their acquiring this technology. This paper proposes governance and policy recommendations for overall water management and, in particular, for future studies and regulation of SPIS-driven groundwater use. Setting appropriate policies for water-pumping powered by renewable energy will help to conserve groundwater sources and sustainably preserve livelihoods

Yemen has experienced unrest for many years, suffering from civil conflicts, wars, a deteriorating economy and severe depletion of water resources.[1] The country’s aridity, limited water resources, and the mismanagement and overexploitation of water contribute to Yemen’s water insecurity. The current war has had a significant impact on water use and the performance of the water and irrigation sectors.[2] Ongoing instability in the country has had negative impacts on the availability of fuel and electricity – energy sources that have typically been used to extract and transport groundwater. As a result of the increased scarcity of electricity and fuel, water resources have been harder to access and water services have become less reliable. Solar energy has started to play a role in providing water to different users, including farmers, who rely to a large extent on groundwater for their agricultural activities. Going beyond generalities, this paper looks in detail at the current uses and potential impact of solar-powered irrigation systems (SPIS) on the sustainability of the use of Yemen’s scarce water.

This study focuses on Sana’a Basin, where the shortage of water is among the most problematic. Of all global national capitals, Sana’a has often been identified as the one most likely to run out of water first.[3] It is important to remember that the hydrology of Yemen varies considerably and therefore findings about Sana’a cannot be assumed to be valid for other basins and regions. However, there are some principles and recommendations of a general nature that are valid across the country. Strategies and detailed policies must, of course, be specific to each basin and region.

None of the official authorities and their related policies/strategies, including the Ministry of Electricity and Energy (MEE), the Ministry of Water and Environment (MWE) and the Ministry of Agriculture, Irrigation and Fisheries (MAIF), have addressed the issues associated with the use of solar energy in Yemen.[4] There are a few studies about solar energy for domestic use,[5] but these have little bearing on the technology’s use for agricultural water extraction. A 2019 UNDP report, the only study so far to discuss the use of SPIS in Yemen, determined the positive advantages of SPIS and promoted its use, but said little about the possible impact of SPIS on groundwater sources.[6]

One of the main issues in water management in Yemen is the considerable groundwater over-extraction, which threatens the viability of life in many parts of the country, as water availability diminishes. One of the problems faced by planners is the complete absence of policies and regulations for the management of new solar energy technologies used for water extraction, but they must also contend with the absence of detailed analysis based on actual field data for SPIS. This paper contributes to reducing this gap. If the over-extraction issue remains unaddressed, the further deterioration of water availability will make life in parts of the country more challenging, if not impossible. With the growing demand for SPIS in Yemen – and given its ability to provide affordable, clean-energy solutions – this paper aims to propose recommendations for governance and donor/financer approaches to the recognition and regulation of SPIS-driven groundwater use.

There are 29 million Yemenis, 70 percent of whom live in rural areas and more than 50 percent of whom depend on agriculture. Yemen has no lakes or permanent rivers: rainfall and groundwater are the main sources of water in the country. Agriculture is estimated to use 90 percent of groundwater resources in Yemen, even though it only generates less than 20 percent of GDP.[7]

Yemen suffers from extreme water scarcity. Per capita water availability has dropped steadily in past decades as known available resources have remained static or have diminished while the population has increased. The annual volume of renewable water per capita declined from 221 m3 in 1992 to 80 m3 in 2014 and to only 75 m3 in 2017;[8] the latter is just over one percent of the global per capita average (5,925 m3) and 14 percent of the Middle East and North Africa region per capita average (554 m3). Yemen’s trajectory over the past three decades suggests available renewable water per capita could drop to 55 m3 by 2030.

According to the internationally recognized Falkenmark indicator, absolute water scarcity occurs if per capita water availability falls below 500 m3 per annum. That is almost seven times the current water availability in Yemen. Since the beginning of this century, Yemen has been using annually one third more water than its renewable supply can support: in 2010, extraction was 3.5 billion cubic meters (bcm) while renewable supply was 2.1 bcm; the 1.4 bcm shortfall was met by water pumped with modern technology from non-renewable fossil aquifers.[9] The groundwater tables have dropped severely, leaving the country in a state of extreme scarcity. For example, in Sana’a Basin, the water table was at a depth of 30 m in the 1970s but had dropped to between 200 and 1200 m by 2012.

There are three main reasons for water scarcity in Yemen. First, rapid population growth, averaging 3 percent per annum, has increased demand thus reducing per capita water over generations. Second, the introduction of diesel-operated pumps and tube well-drilling technology in the past century for irrigation has affected the use of traditional rainwater harvesting systems and enabled extraction of groundwater significantly above recharge levels. This has led to the expansion of agriculture areas and the depletion of aquifers. Third, climate change is manifested through increasingly violent and irregular downpours and other phenomena affecting water availability. These irregular rainfall patterns have further reduced replenishment of aquifers, as the loss of top soil prevents absorption of flows, particularly where terraces and traditional spate systems have deteriorated due to lack of maintenance.[10]

The irrigated area in Yemen has increased from 37,000 hectares (ha) in the 1970s to more than 400,000 ha in the 2000s. During the same period, as irrigated areas increased 11-fold, the area supporting rain-fed agriculture declined by 30 percent.[11] Among the most striking cases of unsustainable water management is the situation in Sana’a Basin, where water resources serve the country’s rapidly growing capital city and high value crops such as qat and grapes. Water extraction there is estimated at five times recharge levels.[12] A further example is that of fruit production in the Tihama: in the middle of Wadi Zabid, a major area for banana cultivation, the irrigated area increased from 20 ha in 1980 to 3,500 ha in 2000. The number of drilling wells increased by more than five times between 1987 and 2008, from about 2,421 to 12,339 wells.[13]

Water management policies and related national institutions have been weak. Farmers with extensive landholdings and powerful social connections have more, and unregulated, access to the resource than small landholders. Following years of benign neglect, the National Water Resources Authority (NWRA) was established in 1995. Officially, NWRA has full authority of water policy development and implementation but, so far, it has been unable to address the complex social and political issues involved in water management.

In July 2002, Law No. 33 of 2002 – known as the “Water Law” – was promulgated. It was amended by Law No. 41 of 2006, but its by-laws were only issued in 2011, demonstrating the intensity of the debate around its implementation. This delay took place despite the fact that the newly created MWE had lost control of agriculture, the most water-intensive sector, in 2003, when the irrigation sector was removed from its authority within weeks of the ministry’s creation and returned to MAIF, the institutional base for large landowners and foreign-financed irrigation development projects.

In 2005, with support from the World Bank and other funders in the water sector, mainly Germany and the Netherlands, the National Water Sector Strategy and Investment Program (NWSSIP) was announced. It was updated in 2008 and contains impressive proposed investments, few of which ever materialized. In January 2011, a Presidential National Conference on Management and Development of Water Resources in Yemen was held, producing a worthy statement of intent. The feasibility of these proposals was never put to the test as the conference was soon followed by the national uprisings and, later in the year, the political transition. NWSSIP, while addressing renewable sources such as rainfall and rainwater harvesting, says nothing about the use of solar energy for water. A further update was made in 2014, though it was not approved by the cabinet due to the political crisis.

In 2013, the total capacity of the national electric grid in Yemen was 1,535 megawatts (MW); 699 MW derived from diesel, 495 MW from steam and 341 MW from gas power plants.[14] The country’s energy needs for lighting alone is estimated at 112 percent of the total generated energy.[15] More than 50 percent of Yemen’s population lack access to the national grid, and the remaining portion experiences frequent power outages.[16] Yemen’s energy policy has largely been focused on diesel and gas electricity generation, which supplied cities, leaving most rural areas without any national links. Yemen has high potential for renewable energy sources – namely, solar, wind and geothermal.[17] However, the country still lacks administrative strategies to promote and regulate the use of sustainable energy resources.

Lack of government action to solve the crisis of basic service provision in Yemen continued during the 2011-14 period while politicians were preoccupied with the political transition and short-term urgent priorities. After 2015, the main immediate impact of the conflict on the majority of urban residents was the interruption of electricity and water services. In rural areas, the main initial impact was the destruction of infrastructure, affecting the inward and outward transport of basic necessities, including agricultural inputs and food. The major fuel crisis that started early in the war decreased energy available for water pumping and, as a result, seriously affected the availability of water for urban households and for irrigated agriculture.

Now, while the war is ongoing, the public water network and electricity grid serve no more than 10 percent of families.[18] All sectors, including agricultural, industrial and services, experience significant increases in input costs for irrigation, transportation and marketing, resulting in lower production and exports.[19] Production has stalled, negatively impacting both public and private sectors. The delivery of public goods and services – including health, education and social security – has been affected throughout Yemen.[20] Fuel and cooking gas prices have become unstable; at times, the cost of these commodities has jumped to more than 1,000 percent from a pre-war baseline.

The war has affected water supply all over the country, in terms of availability, accessibility, quality and affordability. Decentralized, community-based water systems have shown more resilience than public, centralized systems; in many areas, people have gone back to using sustainable techniques, like rainwater harvesting. However, it is worth mentioning that the public water sector is one of very few sectors that have continued to provide services, even if these services are reduced, irregular and reach fewer Yemenis than before the crisis.[21]

The increasing availability and financial accessibility of solar power – combined with the years of intermittent and only occasional electricity service in towns, and even less supply in rural areas – has led to solar energy’s expanded use throughout the country during the war. More than 70 percent of households are now using solar energy as their primary source.[22] Newly installed solar panels can be seen on almost every house in Sana’a (figure 1). Simultaneously, and to some extent with the support of humanitarian agencies, the use of solar-powered pumping to access water has developed considerably throughout the country. This is the case for domestic supply and even more so for irrigated agriculture, though the use of solar for the latter has been financed primarily by well owners and operators, and is thus more available to the wealthier segments of society (figure 1).

Figure 1: Newly installed solar panels on Sana’a houses and SPIS at a farm in Sana’a Basin

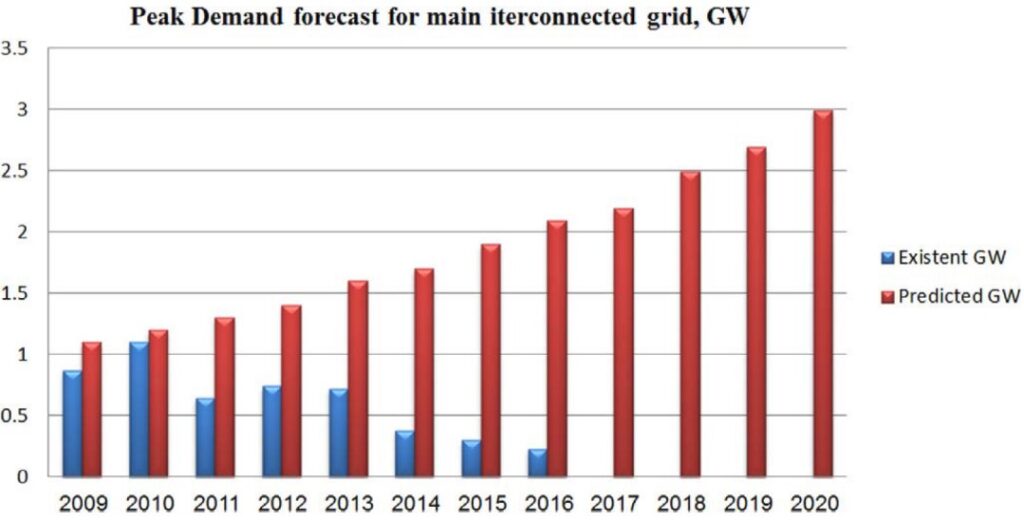

Before the outbreak of the 2011 protests, a 2009-2020 plan to develop and modernize the electric power infrastructure in Yemen was developed by the Public Electricity Corporation (PEC). The plan proposed to increase electricity production to three times 2009 levels, an increase equivalent to 3 gigawatts (GW), to serve factories and new areas and homes that did not have access to the public network.[23] Due to the unrest, all power plants stopped working completely in 2016.[24] Figure 2 illustrates the planned and actually produced electricity over the plan’s time period. The decline in the production of electrical energy began appearing clearly in 2011.[25] Since the war started, the national network has largely ceased to function, replaced locally by small private networks, primarily powered by household-level solar power, though few have enough storage or capacity to operate equipment with high energy demands, such as.[26]

Figure 2: Strategic Electricity Plan up to Year 2020[27]

Solar energy is an eco-friendly, renewable source but many commentators say that it is a double-edged sword in Yemen.[28] While solar pumps can improve access to water and save energy, they might affect aquifers. During the current fuel crisis, many urban public water authorities have begun to use solar-powered groundwater pumping systems to supply domestic water. Using solar pump systems for drinking water supplies has a significant positive impact on water accessibility and, consequently, health and hygiene. However, the use of solar energy for irrigation might lead to over-abstraction of groundwater and add pressure to already stressed water resources. There are around 100,000 pumps in use in Yemen for irrigation purposes.[29] Replacing diesel and electric powered pumps with SPIS without clear rules and restrictions, particularly on qat farms, could lead to the expansion of the cultivation area and, hence, to an unforeseen increase in groundwater abstraction.

SPIS, once installed, has a relatively low cost per unit of power generated. Having said that, farmers try to maximize their use of groundwater in order to recover the high capital costs of the SPIS – either by expanding their irrigated area or by selling water to other farmers. This could lead to a race to the bottom unless regulations are put in place and enforced. Another concern is the drop in costs of solar panel technology. It dropped from around $76/W in 1977 to $0.30/W in 2015. This continuous drop, coupled with increasing diesel prices, has made this type of technology more attractive not only for farmers but also for many decision-makers, funders and technicians. SPIS is an energy-and-water solution that has as much potential to aggravate the water-scarcity problem as to improve the energy-access problem.[30] However, financial incentives to save energy cannot be applied here to avoid wasteful water use. The risks posed by unregulated solar-powered pumping must be identified and addressed, so as to clearly define policies and regulations to mitigate these risks and incentivize sustainable water use.

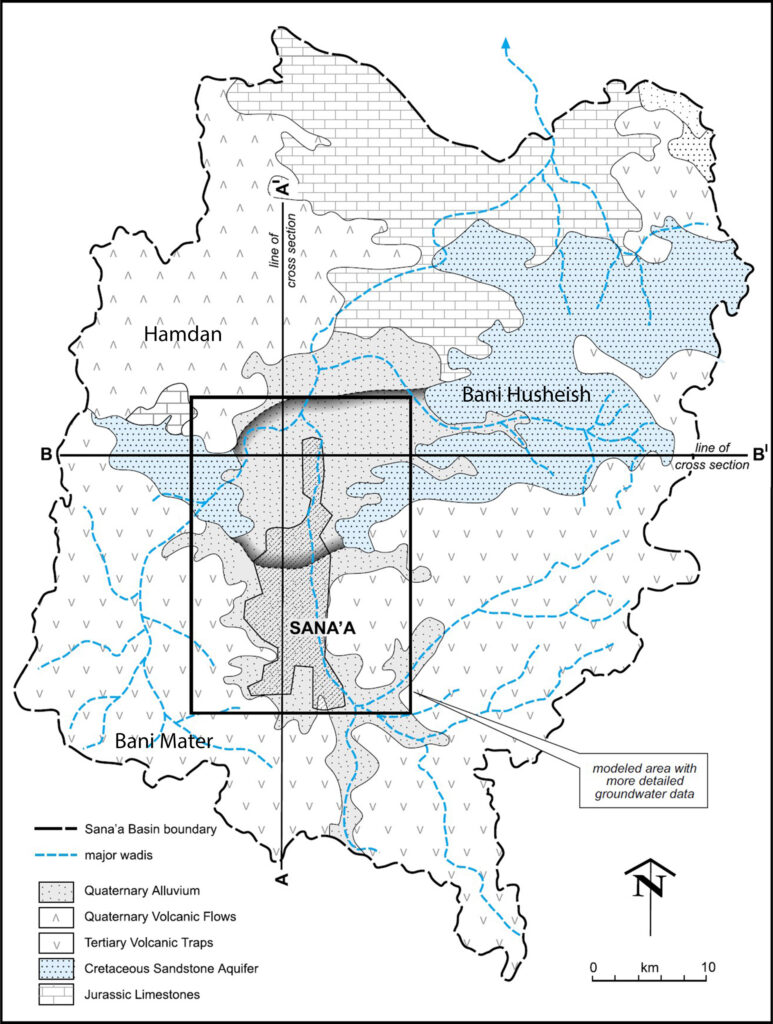

Yemen has 14 water basins. This study focuses on Sana’a Basin (figure 3). Sana’a Basin has 22 sub-basins and spans nine administrative districts, including the Yemeni capital, Sana’a city. The basin has an area of 3,240 km2 and hosts a current population of 4 million.[31] This study’s main unit of analysis is farmers from different hydrogeological areas: Bani Husheish, Bani Mater and Hamdan. The climate of Sana’a Basin is arid and mild throughout the year, with average temperature ranges between 12 and 25° C.[32] Mean annual duration of sunshine per day is 9 hours.[33] Annual rainfall typically ranges between 110 and 350 mm, with an average of 240 mm.[34] However, some years have much higher rainfall, above 350 mm.[35] Rainy days range from 8 to 25 days per year and mainly occur in the two rainy seasons: mid-March to beginning of April and mid-July to end of August.[36]

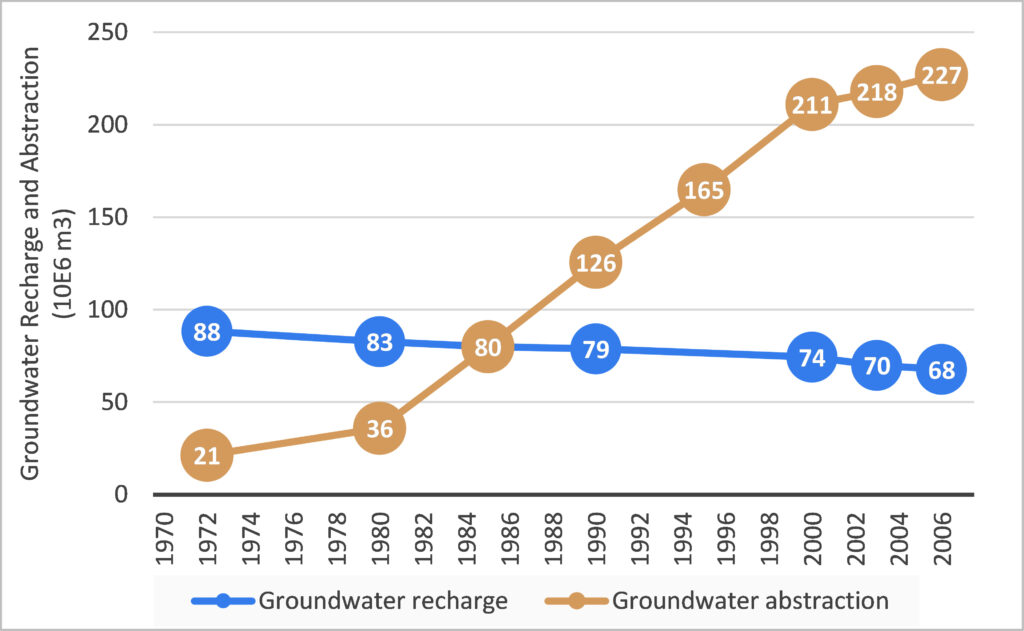

Sana’a Basin relies to a large extent on groundwater for both irrigation and domestic water uses.[37] As a result of rapid population growth in Sana’a city (over 5 percent[38]), uncontrolled immigration and the expansion of agriculture activities, water demand has increased tremendously in the last three decades and new wells continue to be drilled.[39] Today there are more than 13,000 wells in Sana’a Basin. The point of intersection, or balance, between groundwater recharge and abstraction was in 1985, after which groundwater abstraction has kept constantly increasing beyond the basin’s recharge (figure 4).[40] The groundwater aquifers of Sana’a Basin are now suffering over-exploitation. Annual abstraction exceeds 220 million m3, five to six times higher than the volume added through natural recharge, and the water-level decline is about 4-8 m per year.[41] About 90 percent of Sana’a Basin groundwater is used for agricultural activities, with qat and grapes as the most dominant crops.[42]

This study conducted field surveys in December 2020 and January 2021 among a stratified sample of 88 farmers in Sana’a Basin, mainly from Bani Husheish, Bani Mater and Hamdan.[43] The study also undertook key informant interviews (KIIs) with water, irrigation and energy experts to ensure coherence between data at the farmer level and professional- and administrative-level information. This approach facilitated a deeper understanding, from different perspectives, of the future of SPIS, its uses and proper management, in Yemen. After a quality check on the collected data, where needed, participants were contacted by phone to verify unclear or incomplete points.

Sana’a Basin was selected as the study area because it faces water scarcity and has deeper groundwater than other basins; information on the use of SPIS in such a deep basin can be roughly extrapolated to apply to other areas, with the assumption that SPIS use in shallower basins would be easier. However, to cross check, a small sample of data (10 farmers) was collected from Hadramawt, where groundwater depth is <100 m.

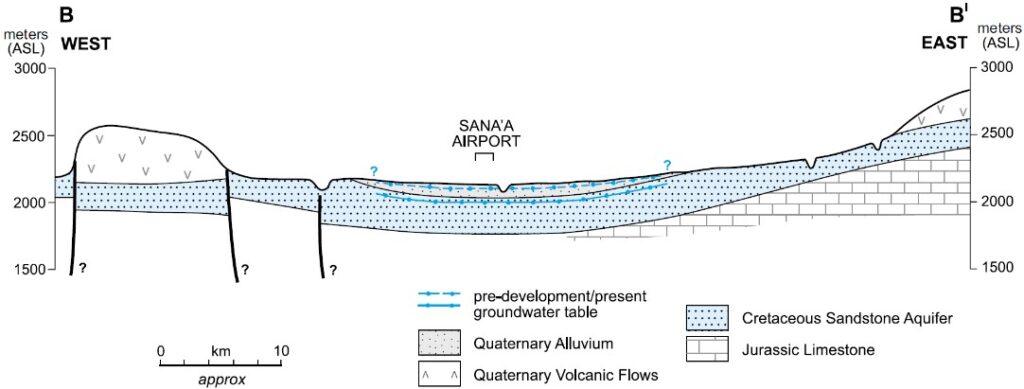

Figure 3: Hydrogeological map and cross-section (B-B) of the Sana’a Basin[44]

Figure 4: Groundwater recharge and abstraction in Sana’a Basin[45]

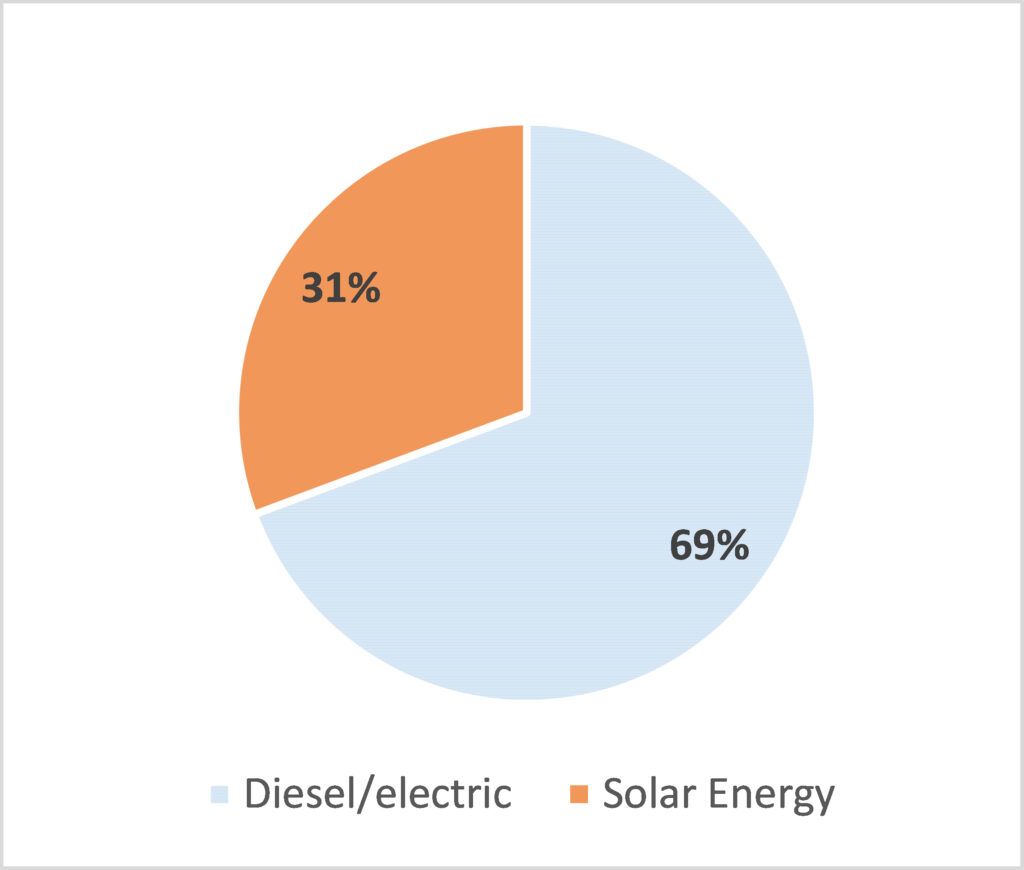

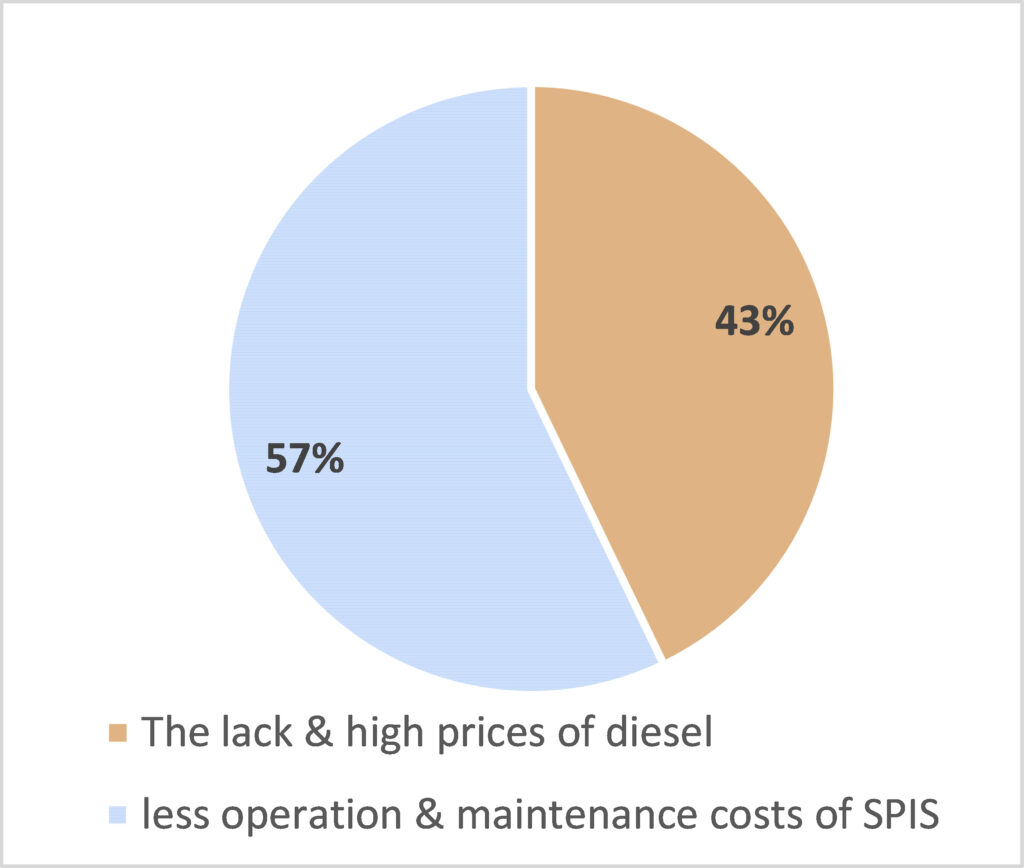

The use of SPIS in Sana’a Basin is dramatically increasing. Today more than 30 percent of farmers in this area are using SPIS (figure 5). This was not the case prior to the current war, when almost all groundwater users in Yemen depended on diesel generators and the electricity grid to pump for irrigation.[46] The early reasons for this shift (2015-2017) were war-related – mainly the lack of electricity in the public network and the scarcity and high price of diesel. Now, and with the growing experience of farmers, the main reason for the shift to solar energy is the lower operation and maintenance costs of SPIS (figure 6) and the fact that it is more reliable than diesel pumps. All users of SPIS report being happy because they can get the quantity of water they used to have and pay almost nothing, bar the capital cost.

|

|

| Figure 5: Sources of energy for irrigation practices (Jan 2021) | Figure 6: Reasons led to SPIS uses (Jan 2021) |

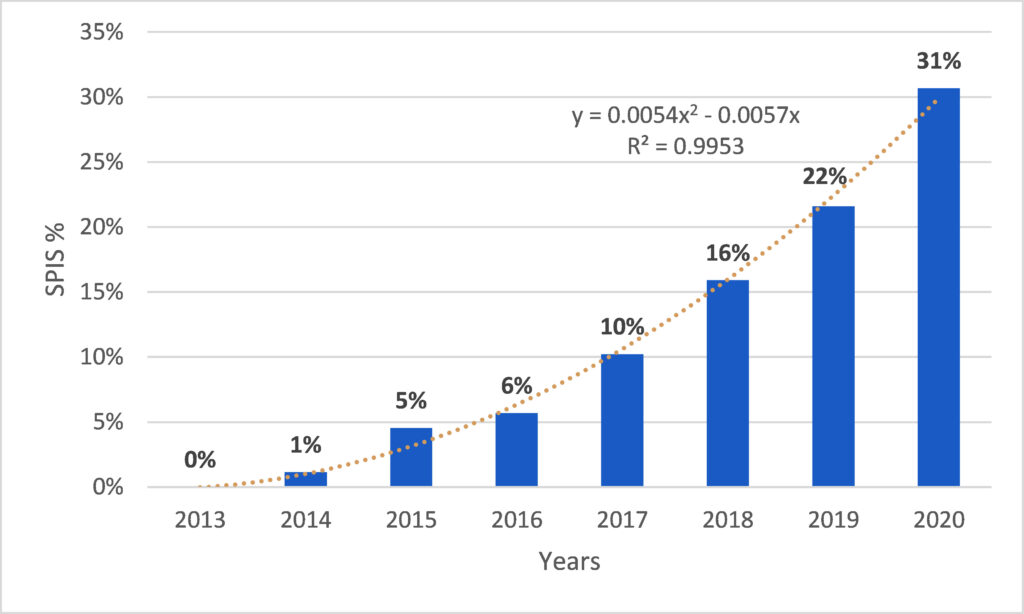

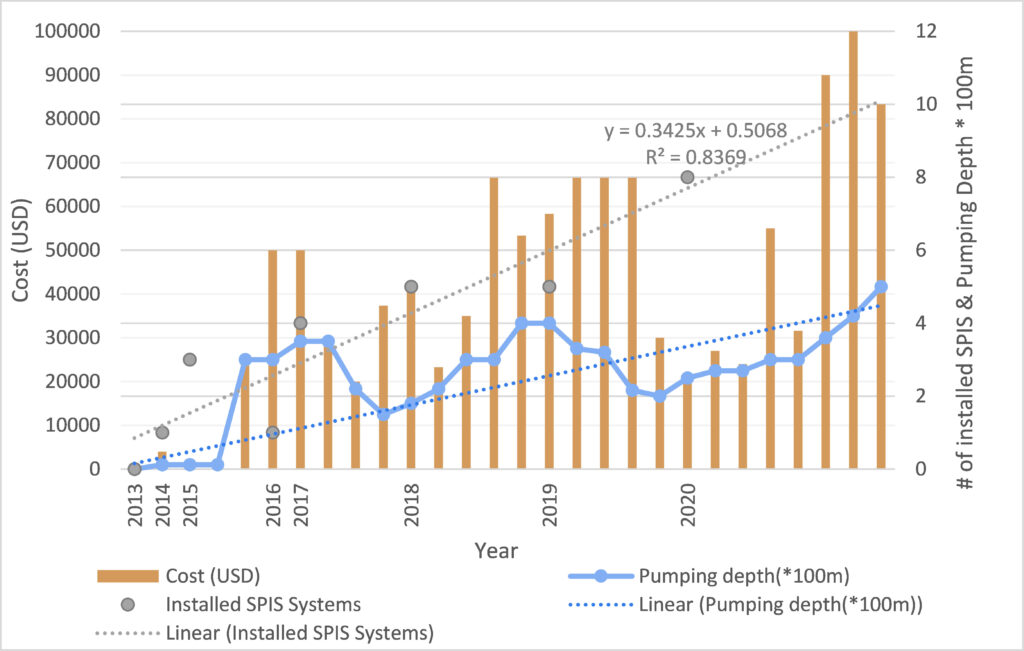

The number of installed SPIS systems is increasing with time. It jumped from 0 percent in 2012 to 12 percent in 2017 to 31 percent by the end of 2020 (figure 7). Likewise, the pumping capacity of SPIS, represented by pumping depth, has witnessed a remarkable development in Sana’a Basin. SPIS use in 2014-2015 was limited to shallow groundwater (<15 m) before increasing to 360 m in 2017 and reaching 500 m in 2020 (figure 8). During the current war and the closure of most Yemeni airports and seaports (particularly in the north), the average uptake of SPIS in Sana’a is increasing by 4.4 percent per year. If this trajectory were to continue, all old pumping systems in Sana’a Basin would be replaced or supported by SPIS within 15 years. If Yemen’s sociopolitical and security situation stabilizes, the conversion to SPIS is predicted to be far quicker; given the experience gained by farmers and the growing solar energy market in Yemen, the country would be expected to witness a complete shift to SPIS within only 7 years.

Figure 7: Accumulative installed SPIS

Figure 8: Installed SPIS, Related Costs & Pumping Depth (2014-2020)

The SPIS installation cost ranges between US$4,000 for shallow groundwater wells and up to US$100,000 for deep groundwater wells (figure 6). The increased depth directly correlates to increased cost; with time, SPIS installation depth and, consequently, costs are increasing. However, the exact relationship between cost and depth is not constant. The quality of the SPIS system (brand and country of origin) and the size (number of solar panels) are also important factors in pricing. Water depth, sun exposure and the system’s efficiency and capacity are the main factors determining pumping capacity. Some farmers said that SPIS secures them water quantities equal to what they used to obtain using other pumps, while other farmers said they obtain even more using SPIS. “Nine hours with the SPIS is equivalent to using a diesel pump from 6 in the early morning until midnight,” a farmer said.

Figure 9: why not SPIS until now?

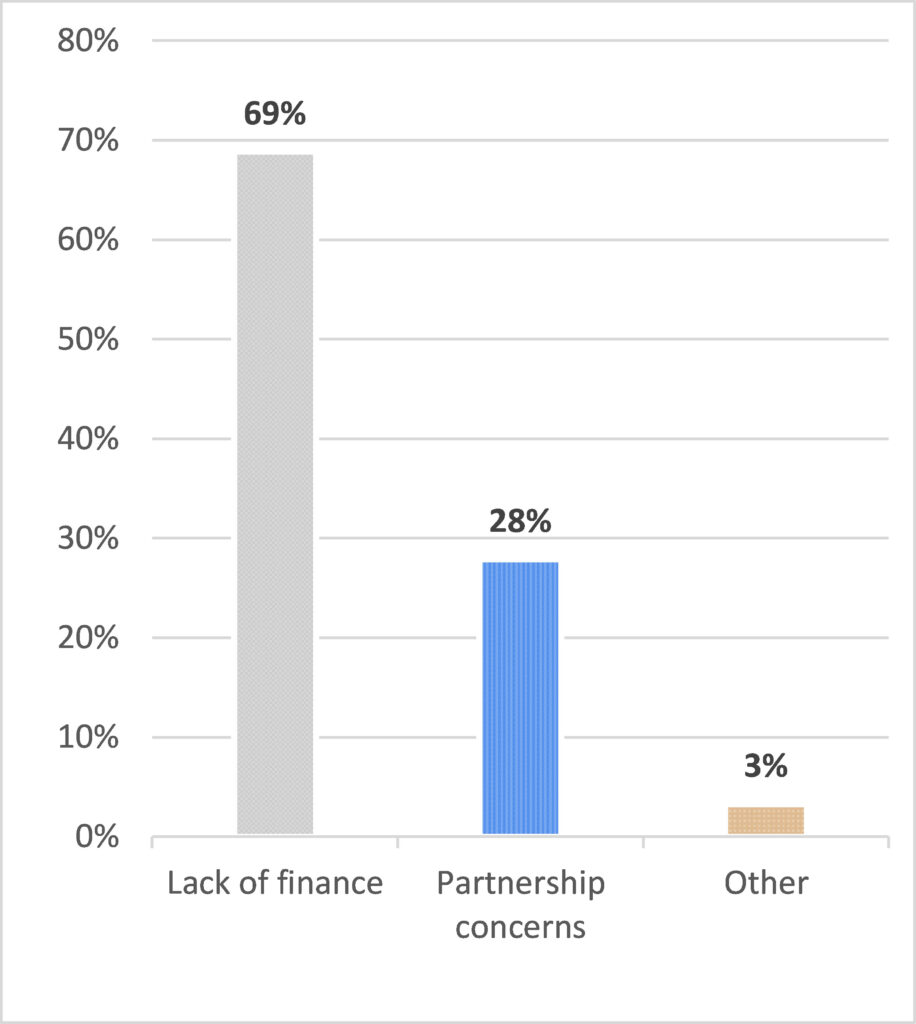

All owners of wells are willing to use SPIS and the main obstacle for most farmers (69 percent) is the capital cost of SPIS. One farmer regretted the opportunity he lost in 2008, when he was offered a free SPIS and refused it. “I was unaware of its advantages,” he said. In a number of areas in Sana’a Basin, farmers share ownership of the wells and pumps. In these areas, local agreements require everyone to share ownership of wells located within their property. When some have no money to pay their share for drilling the well and installing the pump (mostly diesel and electric pumps), other farmers pay in advance for them. The farmers who jointly own wells report facing difficulties replacing their old pumps with solar ones because they use time-based distribution allocations, which is not fully applicable by SPIS. Whereas diesel pumping produces a constant amount of water, variation in solar radiation means that solar pumping can extract different amounts of water. The possible inequity in water quantities obtained in the time allocated means that some joint owners have doubts about introducing solar pumping. Among all farmers surveyed in Sana’a, 28 percent are unwilling to install SPIS due to these partnership concerns and a small minority (3 percent) were not interested in a new SPIS system because they rarely use their traditional pumping systems (figure 9).

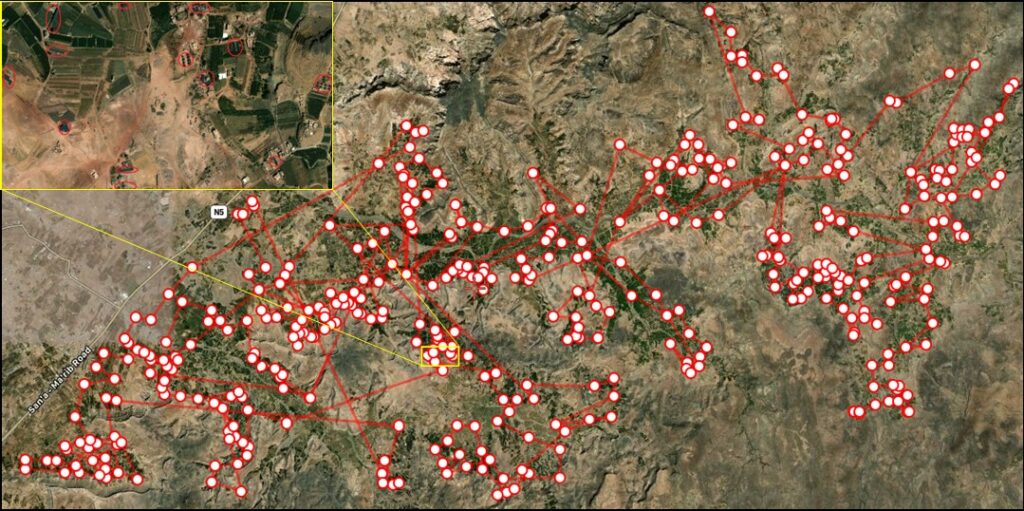

Sandstone and quaternary alluvium areas in Sana’a Basin, such as Bani Husheish, have, for the most part, seen a more drastic increase in SPIS systems as compared with quaternary and tertiary volcanic areas, like Bani Mater. The flat land in Sana’a, such as Bani Husheish, is more fertile than mountainous areas and hosts more rich farmers with qat farms. This significantly helped the spread of solar energy pumps. In Bani Husheish, more than 400 solar pumps had been installed by 2017 (figure 10), approximately 20 percent of the total number of wells in that area.

Among the interviewees there were two farmers using SPIS in both Sana’a and Hudaydah. Although the pumps in Hudaydah cost them less and need shallower pumping depths (30-60 m) than in Sana’a, they are happier with their pumps in Sana’a because the crop there is qat, which is more profitable. The benefits of SPIS in Sana’a outweigh the initial costs because the crops grown there are lucrative. This finding was also supported by the comparative experience of Hadramawt farmers, many of whom have lower financial capacity and have been forced to sell their old pumping systems to cover part of their SPIS costs. In Sana’a, the majority of farmers keep their old diesel/electrical systems and use them as a standby or supplemental system.

Figure 10: Digitizing map of 438 SPIS in Bani Husheish (2017)

As is the case in Sana’a, farmers in Hadramawt prefer SPIS to other pumping systems. The pumping depth in Hadramawt (30-60 m) is more suitable for solar pumps and the use of SPIS has started to spread widely. It is worth mentioning that a number of farmers in Hadramawt have expressed concern about the impact of solar energy technologies on the groundwater levels in the absence of clear regulations and policies. Nevertheless, the Hadrami farmers describe SPIS as a good system with fewer technical problems than electric and diesel systems. The SPIS cost in Hadramawt ranges from US$10,000 to 17,000. The capital cost is the main obstacle preventing most Hadramawt farmers from owning SPIS technology.

The SPIS users in Sana’a and Hadramawt interviewed for this paper received no training on installation, operation or maintenance except a little information about installation from the marketing companies. These users confirmed that they do not have any specific programs or policies to regulate the use of SPIS.

During the current war, farmers have not experienced the kind of drop in groundwater levels experienced before the war.[47] “In the last three years I installed not a single pipe,” one said, indicating that his supply had been sufficient. Long periods of diesel crisis led to a drop in the operating hours of diesel pumps, meaning less water was pumped and, consequently, groundwater resources were under less pressure. Moreover, rainfall in 2019 and 2020 was far higher than usual. “If the rainfall continues as in the last two years we will rarely use groundwater,” a farmer in Sana’a said. SPIS use – while helping to mitigate the challenges posed by the fuel crisis – is not a reason for increased groundwater stability reported by some farmers, primarily because it is still in its early stages. Only 31 percent of surveyed farmers in Sana’a are using these systems. Most of the SPIS adopters are large landholders – those who could have afforded diesel to operate pumps, even in the current fuel crisis.

The diesel crisis is still relevant in early 2021 and many farmers buy diesel on the black market. This study found that the average price of diesel per liter is YR500 and YR325 in Sana’a and Hadramawt respectively.[48] These prices, current as of January 2021, are about five and three times diesel’s pre-crisis price. Since 2011, diesel prices have, at times, reached 15 times their pre-crisis levels. However, with more SPIS systems or increased diesel availability, it is expected that farmers will gradually start to abstract an even greater volume of groundwater than they did in the pre-war period.

Over the course of the conflict, there has been a decline in crop production across the country.[49] The number of qat farms is increasing at the expense of other crops, whose area is diminishing. Wells are being drilled without any involvement of official authorities. “In our area there were more than 200 farmers of crops other than qat; today, there are around 20,” one farmer in Bani Husheish noted. The expansion of qat farms – which, because of the crop’s high water needs, are usually irrigated – increases concerns about the future abstraction of groundwater, especially when Yemen’s situation stabilizes and the availability of SPIS and diesel increases.

There is considerable interest from development actors to support the use of SPIS in Yemen. A number of farmers have already received some support from local organizations (Azal and Al-Wataniah were mentioned by respondents) and international ones (e.g. FAO, IOM, UNDP, CARE, OXFAM and Mercy Corps). Some of these supporting organizations control the maximum depth SPIS can be used for, but this is not always the case. The farmers now know how to get technical support and upgrade these systems. Farmers with large landholdings are able to both buy SPIS systems and access further funds from organizations. Owners of smaller farms face greater barriers to installing SPIS, and some farmers reported that they sold assets like cars and gold in order to buy SPIS. The majority of respondents couldn’t yet afford this technology, although they want it. Solar energy pumps are being promoted and supported by many local and international organizations, on the basis that they save fuel and electricity, protect the environment, reduce CO2 emissions and have health benefits and other social returns. However, there are concerns, mainly from water experts, about the potential impact of SPIS. So far there has been no study in Yemen on what can be done to regulate the use of solar energy, especially in the field of irrigation.

Solar pumps are seen as a potentially powerful solution to government shortcomings in providing electricity grid connections for agriculture. The potential impact of solar pumps on excessive groundwater extraction is generally not seen as a major concern by most policymakers. Farmers are seeing solar pumps as both a pumping and an energy solution. From an economic perspective, any resource that has become easily accessible will inevitably be overexploited, unless access to and use of this resource is restricted through government regulation and policies.

Yemeni energy experts have posited that solar-powered water-pumping might help to conserve groundwater and stabilize water levels, given the time restrictions on pumping (8-10 hours a day) and the limited capacity of these systems. However, no study has systematically assessed these trade-offs. Rather, some studies suggest that the introduction of solar pumps could pose additional risks of over-extraction. The risk that SPIS proliferation is likely to worsen over-exploitation of aquifers is particularly clear given the cautionary tale of historic diesel subsidies, which led to the over-exploitation and dramatic decline of groundwater resources over decades.[50] Increased water wastage has been reported following extensive solar pumping in parts of India and China, for example.[51]

The present study shows that most farmers kept their old pumps to use them at night or when needed. All SPIS owners in Sana’a Basin kept their old pumps (mostly diesel) as standby systems. Others (6 percent) have more than one well and operate both diesel and solar pumping systems. The current users of SPIS rely mainly on solar systems and use diesel pumps only when the SPIS supply is insufficient, mainly during night time in the summer season or on cloudy days. In fact and as mentioned earlier, some farmers have reported abstracting more with SPIS. There is growing evidence that the low operational cost and available energy of SPIS contribute to excessive extraction of groundwater, decreasing water tables and negatively affecting water quality.[52] Yemeni energy experts are supportive of the use of solar energy in all sectors, with their main concern being the quality of imported solar energy equipment, rather than any long-term environmental impact.

Yemeni water and irrigation experts agree and support the use of SPIS in Yemen but in a way that prevents further depletion of scarce groundwater. The use of SPIS minimizes consumption of imported fuel and electricity, alleviates the pressure on the economy (since the Yemeni economy relies, to a large extent, on fuel) and, more importantly, provides a cheaper and ecologically friendlier way of pumping water. This is particularly important in rural areas, where agriculture is the main livelihood option. However, the potential impact of SPIS on groundwater abstraction in the absence of clear policies and regulations cannot be ignored. Therefore, more detailed comprehensive studies on the potential negative impact of SPIS, compared to the traditional fuel-powered systems, are needed.

Although SPIS has limitations of capital cost and pumping time limits, there is still a risk of over-exploitation of groundwater resources associated with the widespread use of SPIS technology, hybrid solar systems and related subsidies. In Morocco, for instance, targeted subsidies for solar pumping have been put on hold due to the government’s growing concern over the depletion of groundwater resources.[53] Another concern is that farmers might irrigate more during the daytime, which lowers irrigation efficiency and water productivity. Most farmers in Yemen are still practicing old methods of flood irrigation and few have modern irrigation systems. These concerns need to be addressed systematically at the community and policy levels, and comprehensive policies and regulations must be prepared. Water experts don’t believe that farmers should be supported with subsidies to cover the capital costs of SPIS, instead advocating for support to be given in the form of technical assistance and capacity building alongside information on sustainable water management.

From the point of view of the farmers surveyed, the main constraints on SPIS expansion include the initial high investment cost, primarily, but also the variable quality of panels, converters and pumps due to the absence of standardization, certification and import controls, worsened in some cases by dishonest dealers.

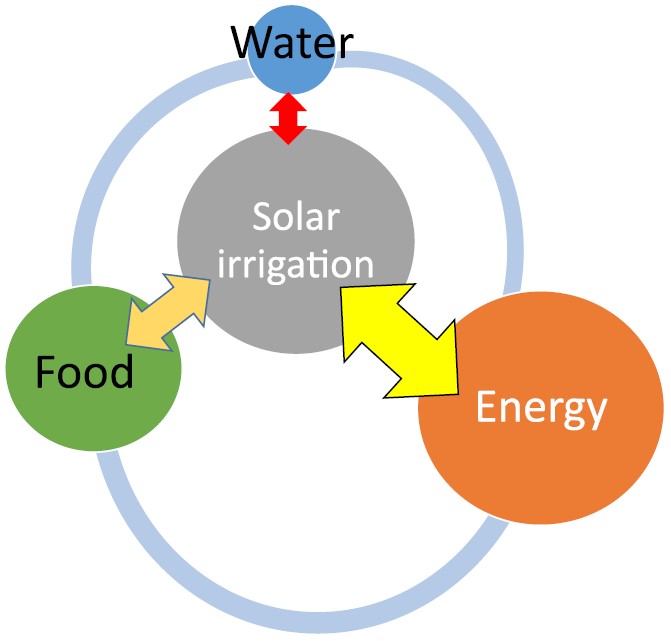

Food security is a challenge in Yemen. But a focus on that challenge should not come at the expense of the country’s endangered water security. SPIS can increase food production by harnessing reliable and sustainable energy to provide timely irrigation. However, these benefits may be at risk as many technical feasibility studies on SPIS fail to appropriately evaluate available water resources and water use and the arising trade-offs within the water-energy-food nexus (Figure 11). Efforts to achieve food security in Yemen should always be linked with water security. Given the large numbers of rural Yemenis and their dependence on agriculture, ensuring the use of the most appropriate and water-saving irrigation technology is very important. However, activating traditional rainwater harvesting systems and developing rain-fed agriculture are of equal importance, as many areas have insufficient groundwater to enable more than very minimal, supplementary irrigation; other areas have none. The most suitable areas for irrigation using SPIS are those with annual rainfall ranging from 300-400 mm, such as Hajjah and Ibb. In all cases, both the benefit of SPIS and the sustainability of groundwater in the area under study should be considered.

Figure 11. The water energy food nexus with SPIS[54]

Although the findings of this study suggest caution in the use of solar power for irrigation, it should be emphasized that its promotion both for the supply of domestic water and of household electricity is an entirely positive development that should be encouraged. Solar power is, in this way, providing basic services to the population, particularly for thousands of rural households throughout the country who would otherwise not have access to these essential facilities.

With respect to sustainable management of Yemen’s scarce water resources, the main finding of this study is that SPIS requires better regulation and management, alongside other water extraction mechanisms, primarily in agriculture, but also for domestic and other uses. The field data collected for this study demonstrates that the use of SPIS has dramatically increased in the last decade in Yemen. The data also shows that the use of solar energy for irrigation in solar-rich and groundwater-scarce Yemen is likely to adversely affect groundwater resources, in the absence of effectively implemented regulations. In other words, SPIS is yet another mechanism that, unless well managed, could contribute to worsening Yemen’s overall water scarcity. The crucial factor determining SPIS attractiveness for farmers is that the marginal cost of solar-powered pumping is almost negligible once they have made the initial investment.

What is also clear is that the cost of a solar irrigation system increases significantly with the depth of the water table. In the case of Sana’a Basin, where wells are deep, costs for installing SPIS reach up to US$100,000. This method of irrigation therefore increases the gap between poor and rich farmers. Even where water can be reached at lesser depths, the price of SPIS installation is still beyond the means of most smallholders. SPIS is more accessible for the wealthiest farmers – those who own other businesses and/or grow the highest value crops.

Overall, it is important to note that all forms of deep-well irrigation are beyond the means of the majority of smallholders. This has a number of implications. First and foremost, farmers can justify irrigating the highest value crops and, more likely than not, they will expand their qat areas at the expense of cultivating basic food crops, such as sorghum. Second, irrigation costs, alongside other economic pressures, are likely to concentrate land ownership even further, as smallholders are forced to sell their assets, thus gradually worsening social differentiation. Policies focused on reducing inequality need to take these factors into consideration when planning water management.

Sana’a Basin is not the only area where aquifers are now very deep; Sa’ada is another. The risk of unsustainable over-exploitation of aquifers and, ultimately, their exhaustion is high throughout the country. Exhaustion of aquifers means not only an end to agriculture but the end of an area being habitable, ultimately leading to forced migration.

Yemen’s formal legal frameworks on water are not fully implemented and, in any case, fail to address the newly introduced SPIS technologies. All legal frameworks and regulations concerning water and energy must be updated to take into consideration the specificities of solar energy technologies, including the use of SPIS. In the short term, it may be difficult to control technology uptake during the war. It is essential that all SPIS users, including the companies and organizations carrying out SPIS installations, increase their understanding of the fragility of water tables. This involves the development of a massive awareness program, which would help to optimize SPIS use and be a good start toward reducing the over-exploitation of aquifers. However, in the medium and long terms, authorities should regulate SPIS and ensure the safe and sustainable use of water resources in Yemen.

Given the current conflict, a number of the recommendations below will only be applicable once effective government has been restored throughout the country. Meanwhile, those which can be implemented should be done so as soon as practicable.

Endnotes

The telecommunications and information technology sector in Yemen is a vital component of the country’s infrastructure and plays a critical role in economic growth. It is the second largest source of public revenue after the petroleum sector, and contributes important work opportunities, whether directly or indirectly, through its connections to other sectors of the national economy.

From 2015 to 2019, the sector’s performance has varied due to the extraordinary circumstances Yemen has been going through. It is estimated that the conflict has caused about $4.1 billion in direct financial losses for the telecommunications sector due to electricity outages (at times caused by a lack of fuel), institutional fragmentation, and competing policies and financial demands by the authorities in Sana’a and Aden, as well as confiscation of assets and extortion. The sector has also lost a number of opportunities that may have otherwise been available if it were not for the outbreak of the conflict, like the development of licensing agreements and the progression to 4G technology. Investors in the telecommunications sector have been deterred from the Yemeni market despite its large size and the fact that many services are not currently being provided by the companies operating in the sector.

The sector faces a large number of challenges, the most serious of which are: the unsuitability of the legal and institutional regulatory environments; fragmentation of public entities in the sector; unproductive accusations made by the parties to the conflict; the lack of separation between political, regulatory and operational roles within the sector; and the reliance on a weak and fragile infrastructure to provide these services. Other challenges include the restrictions imposed on importing equipment, difficulty accessing a number of districts and entire governorates to carry out necessary repairs, declining revenues for the companies, and the increase of fees being levied by both the authorities in Sana’a and in Aden, compounded by the population’s general impoverishment and limited purchasing power.

To strengthen the role of Yemen’s telecommunications, there must be efforts in the short term to depoliticize the sector during the conflict, repair operator networks, introduce new services (such as video conferencing and digital financial services), and work to lower internet tariffs—this paper does not provide an analysis of how to achieve a viable mix of upgraded services and affordable prices while still maintaining the feasibility of new investments. In the medium and long term, efforts to draft new telecommunications laws must continue, in addition to separating regulatory and operational roles, developing the regulatory and institutional environment, encouraging private investment, and updating educational programs and university curricula to ensure that they are up-to-date with ongoing developments in the field of telecommunications and information technology. These curricula and programs must meet the local market’s needs for specialized labor.

The telecommunications and information technology sector in Yemen is a vital component of the country’s infrastructure, and it plays an important role in economic growth. Starting in 2001 and accelerating from 2013 to 2014, the sector witnessed large-scale investments by the private sector as well as the government. Telecommunications towers and infrastructure were installed across much of the country, allowing access to telecommunications services in most Yemeni cities and villages, and there was rapid diffusion of mobile phones and internet services. Prior to 2001, cellular services were provided through the analogue network of a publicly-owned sole mobile operator, TeleYemen.

The sector is of great importance in terms of economic development, social development, and human capital, helping link people, communities, and businesses through the exchange of information in an increasingly connected global economy. It is also one of the most important sources of revenue for the state, especially in acquiring hard currency. Before the conflict, the sector was second only to the oil and gas sector in generating public financial revenues and foreign currency.[1] Mobile operators pay a once-off license fee to the government. During the war, some paid a fee for a temporary license extension until a new full license can be renegotiated. For instance, in 2016, MTN Yemen paid $36.4 million for a 29-month extension to their original 15-year license that was granted in July 2000, thereby extending their operating license to December 2017. In addition, the government collects annual regulatory fees. Generally speaking, governments collect regulatory fees from telecom operators to recover the regulatory costs associated with enforcement, policy and rulemaking, user information, and international activities. For example, MTN Yemen, which held a market share of 42.8% as of 2016 according to their estimates, presumably paid—according to the terms of their license agreement—what would have amounted to YER 1.7 billion annually for the duration of their 15-year license that became effective in July 2000.

Between 2015 and 2018, the telecommunications and information technology sector contributed around 7% to Yemen’s real gross domestic product (GDP).[2] The sector provides employment opportunities directly and indirectly through linkages with other parts of the economy that depend on it.

In addition to the economic and social value of the telecommunications sector, its political, security, and strategic importance cannot be overlooked, whether during wartime or transitional and reconstruction stages. For this reason, the sector has been weaponized by the warring parties. Telecommunications infrastructure has been directly targeted and destroyed by virtually all of the parties to the conflict, while political divisions have deepened institutional fragmentation in the sector, hindering efforts aimed at maintaining or improving its services.

Expanding the telecommunications and information technology sector, realizing its full contribution to economic and social development, and enhancing its competitiveness are areas that hold a lot of potential given Yemen’s relatively large population, high population growth rate, subscriber penetration rates that remain well below 50%, and modest level of services that are currently available. This paper provides a brief presentation and analysis of the mobile telecommunication and internet services that are currently provided, the challenges that the providers of these services face, and the impact of the conflict on the services. The paper then presents several recommendations to enhance and develop the country’s mobile telecommunication and internet services in the short, medium, and long term.

The Ministry of Telecommunications and Information Technology is the government entity mandated with enforcing the laws enacted by the state to regulate the various parts of the sector (i.e., landline telephones, mobile phones, internet, and post). It is also tasked with approving appropriate new bylaws, formulating policies and plans for the sector, managing the frequency spectrum for the mobile broadband services, granting licenses for the establishment and operation of private or public networks, maintaining the national numbering plan, and approving pricing policies for telecommunications services.

Telecommunications Law No. 38 of 1991 Pertaining to Wired and Wireless Telecommunications, as amended in Law No. 33 of 1996, is the sole legislation regulating the telecommunications sector.[3] However, it is not the legal reference point for mobile telecommunications and internet companies and their services in Yemen. Instead, these companies, which started operating several years after technology-specific laws were passed (internet service providers started in 1996 and mobile phone operators started in 2001), are regulated by the licensing agreements that were reached between the government and each network operator.[4] At issue is not so much whether these individual license agreements are standardized in terms of their terms, cost, and procurement procedures, but rather that having an outdated law in place and resorting to piecemeal regulation weakens the legal framework governing the sector and hinders private investment.

The Public Telecom Corporation of the Ministry of Telecommunications and Internet Technology is the only operator for landline services and one of the most important internet providers alongside the Yemen International Telecommunications Company (TeleYemen), which also provides international calling and mobile satellite services.

To help bear the high investment and operational costs of mobile phone companies, and to strengthen the role of the private sector in the economy, the government has incentivized private investment in the telecommunications sector by adopting a wide range of structural reforms. For instance, in 1997, Yemen’s government adopted a program for economic reforms in partnership with the World Bank and the International Monetary Fund (IMF). This program sought to decrease the role of the state in economic life and increase the role of the private sector. As another example of some of the incentives offered by the government, some operators entered into an exclusivity agreement with the government for periods up to four years.[5] As a result, since 2001, the private sector has had an active role in the field of telecommunications. To date, the government has granted three operating licenses to three private companies to operate Global System for Mobile Communications (GSM) networks, namely, Sabafon, MTN Yemen Limited (MTN Yemen) (previously known as Spacetel Yemen), and HiTS Unitel, known by its trading name of Y Telecom. In addition, the government, represented by the Public Telecom Corporation, established a fourth company, Yemen Mobile, which operates a Code Division Multiple Access (CDMA) network.[6]

Table 1: Institutional structure of the telecommunications sector in Yemen

| # | Company | Ownership | Activity |

| 1 | Public Telecom Corporation | Government | Oversees landline telecommunication network, provides services throughout Yemen, including phone, internet and data transmission. |

| 2 | TeleYemen | Government | Provides international telecommunications services, analogue mobile phones, and internet. |

| 3 | Sabafon | Private Sector | Provides GSM services. |

| 4 | MTN Yemen | Private Sector | Provides GSM services. |

| 5 | Yemen Mobile | Government | Provides CDMA services. |

| 6 | Y Telecom | Private Sector | Provides GSM services. |

| Source: National Information Center, https://yemen-nic.info/sectors/information/ (accessed August 28, 2020). | |||

As noted, there are two wireless transmission technologies in Yemen used by local mobile telephone networks. Yemen Mobile, which is majority-owned by the state, provides its services through the CDMA system, while the rest of the carriers use GSM, which was launched for the first time in February 2001. The services provided by these companies are available throughout the Republic of Yemen, although coverage is patchy.

Table 2: Mobile phone services market in Yemen (2019)

| Company | Subscribers in Millions | Market Share | Technology | Ownership |

| Yemen Mobile | 7.5 | 40% | CDMA – CDMA2000 1x – CDMA2000 (2.5G) – 1xEV-DO (3G) | Public Telecom Corporation: 59.37%

Other government entities: 17.3% Private and individual owners: 23.5% |

| Sabafon | 5.2 | 28% | GSM (2G, 2.5G) | Al-Ahmar Group: 60%

Batelco (Bahrain): 26.9% Other investors, including the Iran Foreign Investment Company. |

| MTN Yemen | 5 | 27% | GSM (2G, 2.5G) | MTN Group in South Africa: 83% |

| Y | 0.9 | 5% | GSM (2G) | Formerly owned by Kuwaiti and Saudi investment companies and investors from the private sector in Yemen, the United Arab Emirates, and Syria, the company was purchased earlier in 2020 by al-Essi Group and other Yemeni businessmen close to President Abdrabbuh Mansour Hadi following its bankruptcy declaration in the Commercial Court in Sana’a in March 2020. |

| Source: Public Telecom Corporation, 2019 Report, World Bank, Policy Memo, February 2017. | ||||

From 2015 to 2019, mobile phone services had mixed performance despite the fact that the general trend in this sector has shown positive growth. The overall number of mobile phone connections rose from 15.7 million in 2014 to 18.6 million lines at the end of 2019.[7] Furthermore, by the end of 2018, the unique mobile subscriber penetration rate in Yemen was estimated at 42–43%, compared to a Middle East and North Africa average of 64% and a global average of 66%.[8] The unique subscriber base in Yemen by the end of 2014 was estimated at 46%.[9]

It should be noted that TeleYemen provides mobile-satellite services through its mobile satellite communications service called Thuraya, which enables its customers to use Thuraya phones for voice calls, fax services, and internet connections even when other land-based internet and mobile phone services are not operating. In particular, Thuraya provides essential communication services to oil companies, maritime operations, and development activities in remote areas.

Internet services were introduced to Yemen in 1996 by a single provider, TeleYemen.[10] It owns the country’s International and Internet Gateways (i.e., access to international connectivity via terrestrial and submarine cables). Yemen’s internet is linked to the broader region and the rest of the world through four land and three sea cables. Due to the current conflict, Yemen relies on three working links: (1) The al-Wadiyah land port in Hadramawt governorate, which is a border crossing with the Kingdom of Saudi Arabia, (2) the al-Ghaydhah sea port in al-Mahra governorate, linked to an international submarine cable, the Fibre-optic Link Around the Globe (FLAG) Alcatel-Lucent Optical Network (FALCON) cable, which provides Yemen with the majority of its international links to the internet, and (3) the Aden Port, which is a sea port that is linked to two fiber optic cables, one of which is the Aden–Djibouti submarine cable that has been active since 1994 and was upgraded in 2014. The rest of Yemen’s internet links are not functioning either because of their destruction during the war, as in the cases of the Haradh and Alab land ports along Yemen’s north western border with Saudi Arabia, or because of damage from tropical cyclone Laban, as in the case of the Shihin land port along Yemen’s eastern border with Oman. The fragmentation of policies and institutions among the parties to the conflict has also led to the non-usage of internet links, as in the case of the Asia-Africa-Europe 1 (AAE-1) submarine cable in Aden, in which Yemen invested about $40 million. This link was launched for commercial services in mid-2017. Another example is the FLAG FALCON submarine cable in Hudaydah governorate, in which Yemen invested about $30 million. Once again, Yemen has been unable to use this service since 2017 because of the difficulties encountered in completing the connection through Yemen as a result of the ongoing war.[11]

TeleYemen provides a number of other internet-related services, like web hosting, data transmission, domain name services, and IP address services. Over the past few years, there has been noticeable growth in the number of internet users in Yemen, reaching 7.2 million at the end of 2019, compared to 3.2 million users in 2014. The number of broadband internet (ADSL) subscribers reached 355,058 in 2019 according to the Ministry of Telecommunications and Information Technology (Sana’a), up from an estimated 340,000 in 2014 as estimated by a non-official source.[12] However, when the ministry’s 2019 figure is cross-referenced with available official estimates for the preceding years, we see that the number of subscribers has significantly dropped from 427,699 in 2017 and 385,251 in 2016.[13]

Table 3: Highlights of the makeup of Yemen’s telecommunications market by segment

| 2014 | 2019 | Change | |

| Population[14] | 25,956,000 | 29,665,000 | 14% (+) |

| Unique mobile subscriber penetration rate[15] | 46% | ~42–43% | 4–3 % points (−) |

| Mobile phone connections[16] | 15,708,035 | 18,597,333 | 18% (+) |

| Internet users[17] | 3,236,679 | 7,190,000 | 122% (+) |

| Operated landlines[18] | 1,123,318 | 1,189,397 | 6% (+) |

| Broadband internet subscribers[19] | 340,000 | 355,058 | 4% (+) |

| Sources: CSO, MTIT (Sana’a), GSMA, and ITU. | |||

The prices of these services are one of the main factors in their spread or lack thereof throughout society, taking into account per capita income and educational levels. In this regard, recent studies show that the price of mobile phone services in Yemen is lower than the average price in the Arab world, with Yemen having the 7th lowest price point out of 22 countries in 2017, an improvement of its rank by three positions compared to 2015 and 2016. The price of a bundle of 300 calls was around $56.90 (considering purchasing power parity and value-added tax), compared to an average of around $69.40 in the Arab world.[20]

However, when it comes to mobile data, Yemen is one of the most expensive countries in the world, and the most expensive country in the Arab world, according to Cable.[21] This study compared mobile data prices around the world in 2020, with Yemen ranking last among Arab countries with a single gigabyte costing around $15.98. Somalia provided mobile data for the lowest cost among the Arab states, at an average price of around $0.50 per gigabyte.

Figure (1): The cost of 1GB of mobile data in the Arab world ($/GB

Source: Cable.co.uk, 2020.

According to an estimate by the Ministry of Telecommunications and Information Technology in Sana’a, which is under the control of Ansar Allah authorities, the total wartime losses of the telecommunications sector as of March 2020 are estimated at $4.1 billion due to the damage or destruction of infrastructure, including facilities, telecommunications towers and stations, telephone centrals; confiscation of equipment arriving at Yemen’s ports; and the inability to utilize some of the international internet cables due to the ongoing conflict as earlier noted.[22] Other sources estimate that around 200 out of Yemen Mobile’s 850 transmission stations were not operating as of March 2019 due to the conflict.[23]

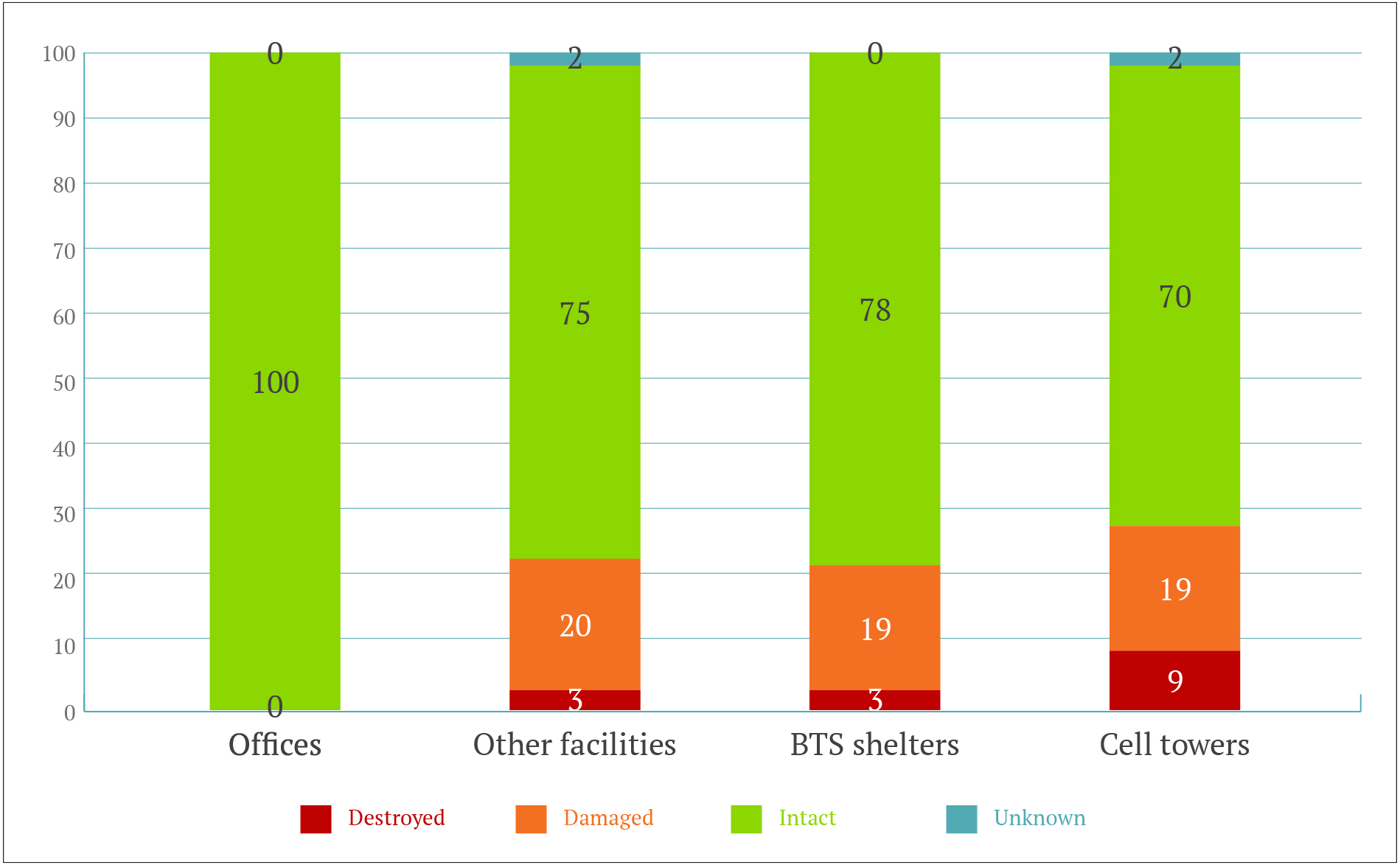

In this regard, the third phase of the World Bank’s Dynamic Damage and Needs Assessment (DNA) estimates that 25% of the telecommunication sector’s assets were either damaged or destroyed since the onset of the war. These estimates are based on satellite imagery, and thus they likely do not capture the full scale of the inflicted damages, particularly because some ICT towers or other facilities such as hangars for telecommunications equipment may not have been visible during the survey. For example, some of the on-ground assessments conducted in the city of Ta’iz suggest that the actual damages largely exceed what was estimated via the satellite survey. Furthermore, the survey does not take into account the ongoing maintenance and re-construction carried out by the different network operators when they have the opportunity to access affected areas. Finally, it is noteworthy that Hudaydah and Sa’ada were the hardest hit governorates in terms of mobile network asset losses, where it is estimated that 75% of the assets in those two areas have been damaged or lost.[24]

Figure (2): Physical damages to the telecommunications sector in Yemen by asset type[25]

Source: World Bank, DNA – Phase 3, 2020.

In addition to the above-mentioned losses, telecommunications companies, especially mobile service providers in the private sector, have experienced losses due to fuel shortages. Companies need fuel to power the generators that provide electricity to their offices, servers, and transmission stations in various parts of the country. Cyclones that have affected some southern governorates have also damaged telecommunications towers and network infrastructure in those areas. All of these factors have reportedly led to a reduction of coverage by around 40%.[26]

Companies have also suffered large financial losses due to institutional and policy divisions and financial demands by the authorities in Sana’a and Aden, as well as the confiscation of assets and extortion by some security agencies and militias. One company, Y Telecom, had to declare bankruptcy in March 2020, leaving behind its equipment and offices in Sana’a and arranging to restart its operations in Aden using 4G technology.

From January to March 2020, there was a wide scale internet outage in Yemen due to damage to the FALCON cable near the Suez Canal. The internet outage disrupted commercial business activity, internal and external financial transfers, as well as other official and private communications throughout Yemen.

Another result of the war has been the loss of opportunities to develop and modernize Yemen’s telecommunications technologies. Many of the licensing agreements with companies operating in the sector were nearing expiry just before the war started in 2015. Renegotiated licenses would have enabled these companies to provide next-generation mobile internet services.[27] Only the state-owned mobile phone company Yemen Mobile has been granted permission to provide mobile internet services using 3G technology.[28] The rest of the mobile telecommunications operators have only been granted licenses by the Ministry of Telecommunications and Information Technology to provide 2G or 2.5G mobile internet services, which have a limited capacity.[29] Restrictions preventing these companies from developing their technology and services result in indirect losses to the companies, the telecommunications sector in general, and consumers.[30] Another source of indirect losses is the fragile, complicated, and high-risk investment environment, which has discouraged investors from entering the Yemeni market, despite its large size and the plethora of services that are not being provided by companies currently operating in the sector.

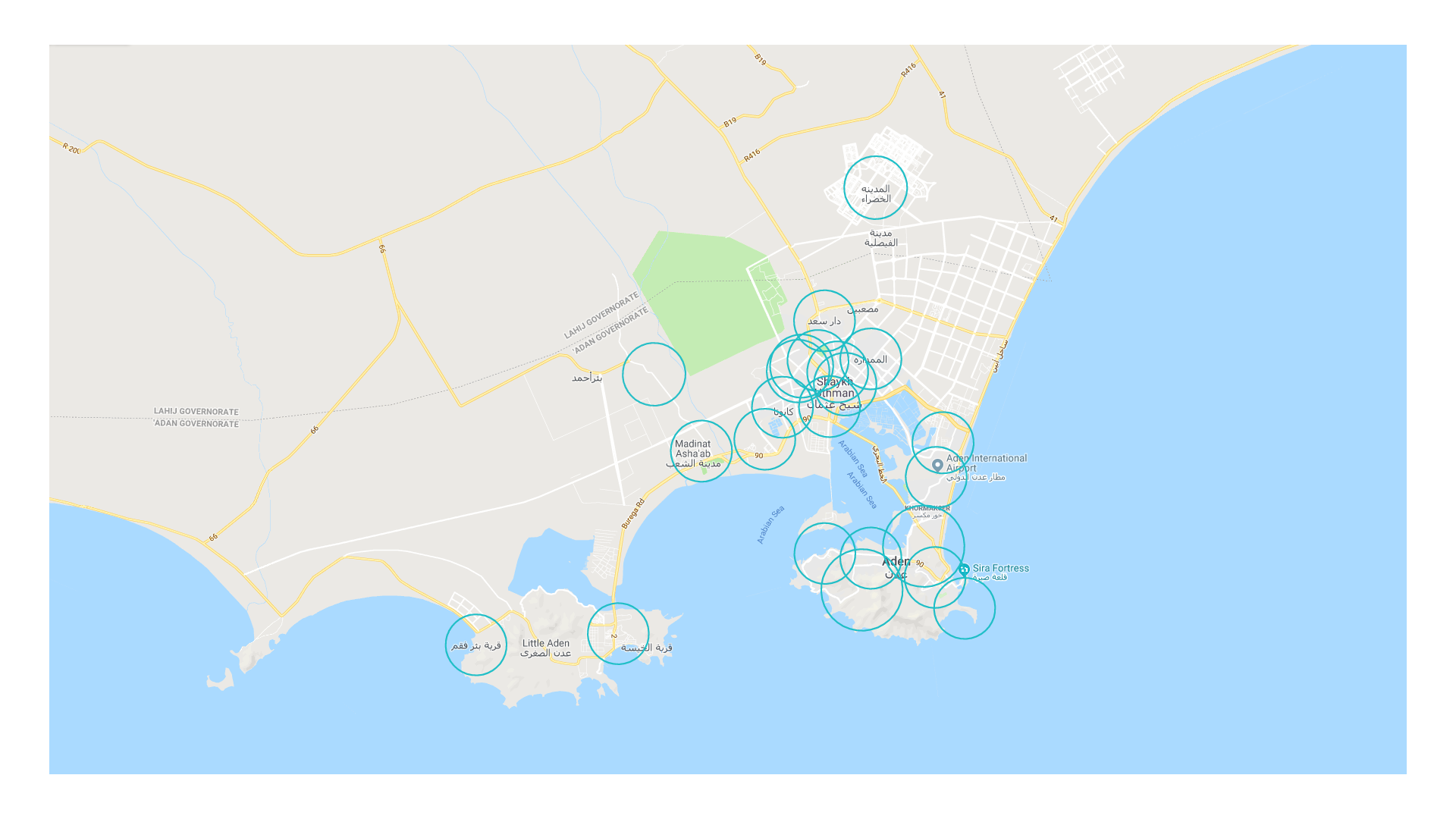

The continuing conflict risks deepening the institutional divides in the various vital economic sectors, including telecommunications. For example, the internationally recognized government has opened a new portal for the provision of internet services called Aden Net, using 4G technology.[31] Both Sabafon and Y Telecom have been preparing to shift to 4G through this new portal.[32]

Figure (3): Aden Net coverage[33]

Despite the conflict’s destruction and the challenges, it has created for the operating environment, the new political, economic, and social reality it has imposed has also created new opportunities in the telecommunications and information technology sector. For example, there has been an increase in demand for internet services, especially due to the electricity outages whereby many consumers have become reliant on access to the internet to follow news and developments affecting their daily lives. The increased demand for these services has led to:

This policy brief was prepared for the Rethinking Yemen’s Economy project by DeepRoot Consulting, in coordination with project partners Sana’a Center for Strategic Studies and CARPO – Center for Applied Research in Partnership with the Orient

Endnots

[1] (i) Naoko Kojo and Amir Althibah, Yemen Monthly Economic Update, January 2020 issue, World Bank Group, January 2020, p. 6: “the [telecom sector] was second to the oil and gas sector in terms of bringing in foreign currency and as a source of fiscal revenues,” http://pubdocs.worldbank.org/en/901061582293682832/Yemen-Economic-Update-January-EN.pdf (accessed August 28, 2020). (ii) Naomi J. Halewood and Xavier Stephane Decoster, “Input to The Yemen Policy Note no. 4. on Inclusive Services Delivery: Yemen Information & Communication Technology (ICT),” Washington, D.C.: World Bank Group, February 13, 2017, p. 4: “Prior to 2015, government revenue from the telecommunications industry was said to be second largest after hydrocarbons. Moreover, telecommunications services brought in hard currencies into the economy, previously reported in the order of about USD300 million, annually,” http://documents.worldbank.org/curated/en/337651508409897554/Yemen-information-and-communication-technology-ICT (accessed August 28, 2020).

[2] Central Statistical Organisation (CSO), “Statistical Year Book for 2017 – Chapter 25: National Accounts,” Table 10 (“The Structure of GDP at Producers Prices by Economic Activity at Constant Prices for 2004–2017 (%) 2000=100”) in Excel sheet labelled “10,” http://www.cso-yemen.com/publiction/yearbook2017/National_Account.xls (accessed August 28, 2020). According to the cited table, the ICT sector’s share (including both the public and private sectors) of national real GDP in 2015, 2016, and 2017 is 6.69%, 6.96%, and 6.88% respectively.

[3] Law No. 38 of 1991 Pertaining to Wired and Wireless Telecommunications as Amended in Law No. 33 of 1996, https://www.wto.org/english/thewto_e/acc_e/yem_e/WTACCYEM4A1_LEG_16.pdf (accessed October 13, 2020).

[4] Ibid. See Paragraph K of Article 3 for reference to licensing agreements.

[5] MTN, “MTN Investors Group Note 35: License Agreements,” MTN Yemen license agreement: “The licence agreement is effective from July 2000 and is applicable for 15 years, renewable thereafter. There is a four year exclusivity clause after which licence parity will apply,” http://www.mtn-investor.com/mtn_ar08/book2/fin_gr_notes35.html (accessed November 17, 2020).

[6] GSM is a 1990s standard developed to describe the protocols for second-generation (2G) digital cellular networks used by mobile devices such as mobile phones and tablets. By the mid-2010s, it became a global standard for mobile communications, achieving over 90% market share, making GSM the most ubiquitous of the many standards for cellular networks, including the CDMA standard of the same era. For more technical details about the different generations of cellular standards, see: Kgs Venkatesan, “Comparison of CDMA and GSM mobile technology,” Middle East Journal of Scientific Research 13(12):1590-1594, January 2013, https://www.researchgate.net/publication/273452419_Comparison_of_CDMA_and_GSM_mobile_technology (accessed October 16, 2020).

[7] (i) For the 2014 figure, see: Central Statistical Organisation (CSO), “Statistical Year Book for 2016 – Chapter 13: Communications & Information Technology,” Summary table (“Main Statistical Indicators of Communications and Information Technology”) in Excel sheet labelled “Indicators [AR],” http://www.cso-yemen.com/publiction/yearbook2016/Communication_Information_Technology.xls (accessed August 28, 2020). (Original source: Annual Statistical Bulletin of Public Corporation for Wired and Wireless Telecommunications of 2016.) (ii) For the 2019 figure, see: Ministry of Telecommunications and Information Technology (MTIT) (Sana’a), an infographic on the homepage entitled “Telecommunication and Information Technology Infrastructure Indicators 2019 [AR],” http://www.yemen.gov.ye/portal/portals/4/upload/%D8%A7%D9%86%D9%81%D9%88%D8%AC%D8%B1%D8%A7%D9%81%D9%8A%D9%83/1.jpg (accessed August 28, 2020).

[8] GSM Association (GSMA), “The Mobile Economy: Middle East & North Africa 2019,” 2019, pp. 2: “For context, the global average at the end of the same period was 66%,” 4, and 9 (Figure 2: The GCC Arab States lead the region in terms of subscriber penetration (Q2 2019)), https://www.gsma.com/mobileeconomy/wp-content/uploads/2020/03/GSMA_MobileEconomy2020_MENA_Eng.pdf (accessed August 28, 2020). Note that unique subscriptions differ from mobile connections—a single subscriber can have multiple connections (i.e., active mobile phone numbers/SIM cards). However, the details of GSMA’s methodology for calculating unique penetration rates are unknown.

[9] GSM Association (GSMA), “The Mobile Economy: Arab States 2015,” 2015, p. 8 (Figure captioned “Arab States penetration by country (Q2 2015)”), https://data.gsmaintelligence.com/research/research/research-2015/the-mobile-economy-arab-states-2015 or https://data.gsmaintelligence.com/api-web/v2/research-file-download?id=18809327&file=the-mobile-economy-arab-states-2015-1482139932360.pdf (accessed August 28, 2020).

[10] TeleYemen has been the sole licensed provider of the international telecommunication services in Yemen since 1972. It was established as a subsidiary company of the British company “Cable & Wireless plc” C&W, until 1990 when the Yemen Public Telecom Corporation (PTC) became a partner with C&W with a 49% of the total shares and then the company’s name changed to TeleYemen. In 2004, TeleYemen became a 100% state-owned entity with 75% of shares owned by PTC and 25% owned by the Yemen Post & Postal Savings Corporation.

[11] “An Economic Expert Interviews the Minister of Telecommunications on the Future of Telecom Companies’ Business Activity and Whether or Not They Are Being Targeted [AR],” Aden Time, February 17, 2020, http://aden-tm.net/NDetails.aspx?contid=117958 (accessed August 28, 2020).

[12] See Table 3 for detailed citations of all these 2014 and 2019 figures and others.

[13] Central Statistical Organisation (CSO), “Statistical Year Book for 2017 – Chapter 13: Communications & Information Technology,” Summary table (“Main Statistical Indicators of Communications and Information Technology”) in Excel sheet labelled “Indicators [AR],” http://www.cso-yemen.com/publiction/yearbook2017/Communication_Information_Technology.xls (accessed August 28, 2020). (Original source: Annual Statistical Bulletin of Public Corporation for Wired and Wireless Telecommunications of 2016.)

[14] Central Statistical Organization (CSO), “Projections for 2005-2025,” June 2010.

[15] (i) For 2014 data, see: GSMA, “The Mobile Economy: Arab States 2015,” op. cit. (ii) For 2019 data, see: GSMA, “The Mobile Economy: Middle East & North Africa 2019,” op. cit. Recall that unique subscriptions differ from mobile connections

[16] (i) For 2014 data, see: CSO, “Statistical Year Book for 2016 – Chapter 13: Communications & Information Technology,” op. cit. (ii) For 2019 data, see: MTIT (Sana’a), “Telecommunication and Information Technology Infrastructure Indicators 2019 [AR],” op. cit.

[17] Ibid.

[18] Ibid.

[19] (i) For 2014 data, see: International Telecommunication Union (ITU), ICT-Eye (online database), https://www.itu.int/net4/ITU-D/icteye/#/query (accessed August 28, 2020). Official data not available for this year because until 2014, available official statistics by TeleYemen and the Public Telecom Corporation used to combine ADSL and dial-up internet subscriptions (See: CSO, “Statistical Year Book for 2016 – Chapter 13: Communications & Information Technology,” op. cit.). (ii) For 2019 data, see: MTIT (Sana’a), “Telecommunication and Information Technology Infrastructure Indicators 2019 [AR],” op. cit.

[20] Nasser Al-Fadhel, “Comparative Study of Communication Prices in Arab Countries,” 16th Annual Arab Regulators Network (AREGNET) Meeting, Manama, October 2018.

[21] Cable.co.uk, “Worldwide mobile data pricing: The cost of 1GB of mobile data in 228 countries,” https://www.cable.co.uk/mobiles/worldwide-data-pricing/#regions (accessed August 29, 2020). According to the source, data from 5,554 mobile data plans in 228 countries were gathered and analyzed between February 3–25, 2020. The average cost of one gigabyte (1GB) was then calculated and compared to form a worldwide mobile data pricing league table.

[22] Ministry of Telecommunications and Information Technology (MTIT) (Sana’a), an infographic on the infographics web page, http://www.yemen.gov.ye/portal/Portals/4/upload/%D8%A7%D9%86%D9%81%D9%88%D8%AC%D8%B1%D8%A7%D9%81%D9%8A%D9%83/%D8%AC%D8%B1%D8%A7%D8%A6%D9%85%20%D8%A7%D9%84%D8%B9%D8%AF%D9%88%D8%A7%D9%86.jpg (accessed August 28, 2020).

[23] “Between Houthi Extortion and Government Failure.. Yemen Telecommunications Fight to Survive [AR],” al-Khaleej Online, March 22, 2019, http://khaleej.online/64z4Ba (accessed August 28, 2020).

[24] World Bank, Dynamic Damage and Needs Assessment (DNA) – Phase 3, 2020, pp. 91–100.

[25] BTS shelters are small shelters at the base of towers that house a device called the base transceiver station (BTS), a piece of equipment that facilitates wireless communication between user equipment and a network.

[26] Al-Khaleej Online, op. cit.

[27] The licenses granted to the two largest operators in the private sector (MTN Yemen and Sabafon) expired in 2015, and there have been negotiations since that time to extend them temporarily until new licenses can be negotiated. For instance, MTN’s most recent financial reports indicate that MTN Yemen was granted a new short-term extension on January 1, 2020, for 900MHz and 1800MHz licenses for two years (see: MTN Group Limited, “Annual financial statements for the year ended 31 December 2019,” March 11, 2020, p. 72, https://www.mtn.com/wp-content/uploads/2020/04/MTN-Annual-financial-statements.pdf (accessed December 2, 2020)).

[28] As noted, the Ministry of Telecommunications and Information Technology is responsible of issuing licenses. In 2004, Yemen Mobile took over TeleYemen cellular network and replaced its analogue services with CDMA services and was granted a 3G license by the ministry.

[29] As noted, licenses are granted to mobile operators by the Ministry of Telecommunications and Information Technology (MTIT). Before 2015, there were negotiations between the ministry and mobile operators like MTN Yemen and Sabafon for the renewal of their licenses and migration of their networks to 4G. At that time, the operators’ point of view was that they were already licensed to operate and they should only have to pay fees for the new 4G services, whereas the ministry’s point of view was that 4G was an entirely new offering that requires a different kind of equipment and infrastructure. Thus, according to the ministry, a new license is needed, not just new fees. At any rate, all discussions regarding migration to 4G came to a halt post-2015 due to the wartime blockade that has prevented any new telecom equipment from entering the country.

[30] Halewood and Decoster, op. cit., p. 2: “Only the state-owned mobile operator, Yemen Mobile was provided permission to provide 3G services. The others only had licenses to offer 2G or 2.5G services, with 2.5G allowing for very limited data capacity.”

[31] The performance of Aden Net is still lagging behind, and its coverage is limited to some districts in the governorate of Aden only. Furthermore, it conducts its business in a monopolistic manner. For instance, Aden Net is the only seller of Aden Net internet modems. Furthermore, because of its limited financial resources, it is unable to supply them in sufficient quantities. This has resulted in very high internet prices that are beyond reach for most people, in addition to creating a new black market for selling these modems.

[32] In September 2020, Sabafon announced launching its operations from Aden to offer its services to areas under the internationally recognized government’s control via a network that is technically and administratively independent from Sana’a.

[33] Aden Net, “Coverage Map [AR],” https://www.adennet4g.net/index.php/ar/2018-07-17-07-54-46 (accessed October 16, 2020).

[34] The local networks are established in neighborhoods, cities, towns, and rural areas. They are wi-fi networks whose operators subscribe to the Super Net service from Yemen Net, the dominant Internet Service Provider, and then provide internet services through prepaid cards.

[35] Casey Coombs, “In Yemen, the internet is a key front in the conflict,” Coda, March 10, 2020, “Houthi government in Sanaa announced that it would no longer issue business permits to the community networks”, https://www.codastory.com/authoritarian-tech/yemen-internet-conflict/ (accessed August 28, 2020).

[36] Sharaf al-Kibsi and Mustafa Hantoush, “WhatsApp in War-Torn Yemen Opens Opportunities to Improve Resilience, Livelihood, and Prosperity Through Microfinance Communication Innovation,” National Microfinance Foundation, March 2018, https://www.findevgateway.org/sites/default/files/publications/files/whatsapp_in_yemen_microfinance_v2_0.pdf (accessed August 28, 2020).

[37] Small & Micro Enterprise Promotion Service (SMEPS), “Yemen Rapid Business Survey 2019” (unpublished).

[38] As already noted, until 2014, available official statistics by TeleYemen and the Public Telecom Corporation used to combine ADSL and dial-up internet subscriptions—not users, because statistics differentiate between internet users in Yemen and subscribers to the different internet services available in the country, namely, ADSL and dial-up—putting the combined total for 2014 at 998,856 (See: CSO, “Statistical Year Book for 2016 – Chapter 13: Communications & Information Technology,” op. cit.). However, by subtracting the ADSL-only subscriptions estimated in Table 3 at 340,000 in 2014 from this total figure of 998,856, we estimate that the total dial-up subscriptions in 2014 would have amounted to 658,856 subscribers.

[39] Abdulqadir Othman, “Internet in Yemen: The Nightmare of War and the Curse of Monopoly [AR],” The New Arab, December 15, 2019, https://www.alaraby.co.uk/medianews/d7a9b457-9681-47b4-abcc-249fca044438 (accessed August 28, 2020).

[40] Halewood and Decoster, op. cit., p. 3: “In December 2015, there were an estimated 16.88 million mobile customers in Yemen, down 4.2% from 17.62 million a year earlier and a recent peak of 18.36 million at the beginning of 2015 […] the impact of conflict on mobile penetration rates is almost immediate.”

[41] MTN Group Limited, “Results overview for the year ended 31 December 2019,” March 11, 2020, p. 28: “MTN Yemen also contributed positively to the MENA portfolio, growing service revenue by 14,2%* on the back of a 28,8%* increase in data revenue against a challenging macroeconomic backdrop and political instability,” https://www.mtn.com/wp-content/uploads/2020/03/MTN-Group-2019-annual-results.pdf (accessed December 2, 2020).